Lifecycle Investing - The New Free-ish Lunch

Investors can dramatically improve their returns by slightly increasing their risk and stock allocation.

This is a follow-up to Invest Time. I recommend reading that first.

My initial post on why most young adults shouldn't have fixed income

In my initial post, I argued that most young adults should be 100% invested in stocks. Since then, I've chatted with several colleagues and subscribers who agreed that young adults being 100% in stocks isn't radical at all. Given the newsletter's audience, I've decided to further discuss why 200% in stocks isn't that extreme either. In today's notes, I'll try to summarize some parts of Ian Ayres & Barry J. Nalebuff's brilliant book - Lifecycle Investing, but I highly recommend reading it. This book has an expiration date for the reader, depending on how much time they have left to invest.

Leverage & Wealth

Let's revisit this idea of diversifying across time (temporal diversification, as the book calls it). The goal is for you to try to spread out your exposure to the market over several decades.

People make the mistake of putting 80 percent of their stock investments in just ten years. This can have disastrous consequences if those ten years happen to end badly. In fact, as we write this in the summer of 2009, the S&P stands at its 1997 level. People close to retirement who invested the bulk of their stock money in this lost decade will not have done well. You are better off spreading your stock investments across several decades.

But as a young adult, you probably don't have enough money to diversify your portfolio properly. Your portfolio can be 100% in stocks using just your own money, but you'll need to borrow the other half to get to 200%. Now, most people stop listening or reading, in this case, whenever leverage comes into play. Borrowing money is sometimes scary, and investing borrowed money is taboo for most. But this isn't Dave Ramsay's notes. Leverage plays a big part in building wealth, and borrowing can be beneficial or disastrous depending on how the money is borrowed and what it's used for.

For example, let's look at a mortgage – people are okay with putting up to 20% down on a new property and borrowing the rest. What's unheard of is a real estate investor that pays cash for every single property they invest in. If you buy a $100k home with $10k down, you'll be levered 10:1. If that home's value increases by 10%, your equity also increases, but by 100%. The same goes for downturns - a 10% decrease in the scenario above wipes out all the equity you have in that property in the short term. This translates over to stocks, though we'll never be levered 10:1. You can still leverage your positions in stocks without borrowing anything if debt scares you, but everything has a cost.

Levering Up

The book suggests a 2:1 leverage for the first decade of your working life. After that, gradually lever down till your mid-fifties. Finally, start to fully unlever while replacing portions of the portfolio with fixed income. As a young adult, you're probably in the first stage. You can leverage with margin, levered ETFs, or options. With margin, you're borrowing money from your brokerage, and they'll charge interest on the money till it's paid back in full. It is the easiest way to get closer to 2:1 but beware of margin calls.

Some levered ETFs, such as ProShares Ultra S&P500 (SSO), try to return 2x the daily performance of the S&P500 before fees and expenses. If you go this route, beware of decay & volatility. Simply put, if the index goes up 10% from 100 to 110, your levered ETF position goes from 100 to 120. If the index then drops 9%, from 110 back down to 100, the levered position drops from 120 to 98.4. You end up with $2 less than you started with. I don't recommend levered ETFs due to the decay on top of their expense ratios.

Options, on the other hand, get a bad reputation. They can actually be used to lever your portfolio without directly borrowing money. Deep in the money LEAPs with a strike price roughly half of the index can be used to achieve 2:1 leverage. As of writing, SPY is trading at $333. You can get a Jan 21, 2022, 165 Call for $170. Remember that an option grants you the right to purchase 100 shares at the strike price. You're essentially paying a little more for this right. In our example, this option will cost $170 * 100 shares or $17,000, but it exposes you to about $34,000 worth of SPY returns. This is my preferred way of levering.

Lifecycle Investing

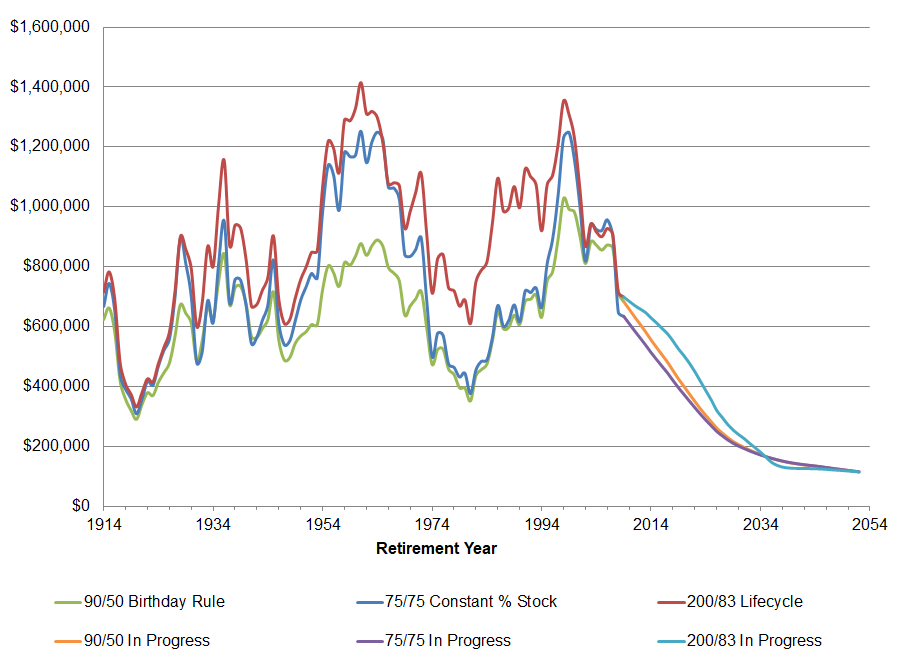

The lifecycle strategy recommends starting at 200% in stocks, and levering down to 83% stocks at retirement. Compared to more traditional strategies like 90/50 target date (90% stocks now, 50% stocks at retirement) and constant 75% stocks, the 200/83 lifecycle strategy performs extremely well from a return and risk perspective. The authors of the book ran 96 different historic simulations on a theoretical investor that was invested for 43 years starting from 1871 - 1914, 1872 - 1915, till 1966-2009. They found that you can dramatically increase your returns by taking slightly more risk.

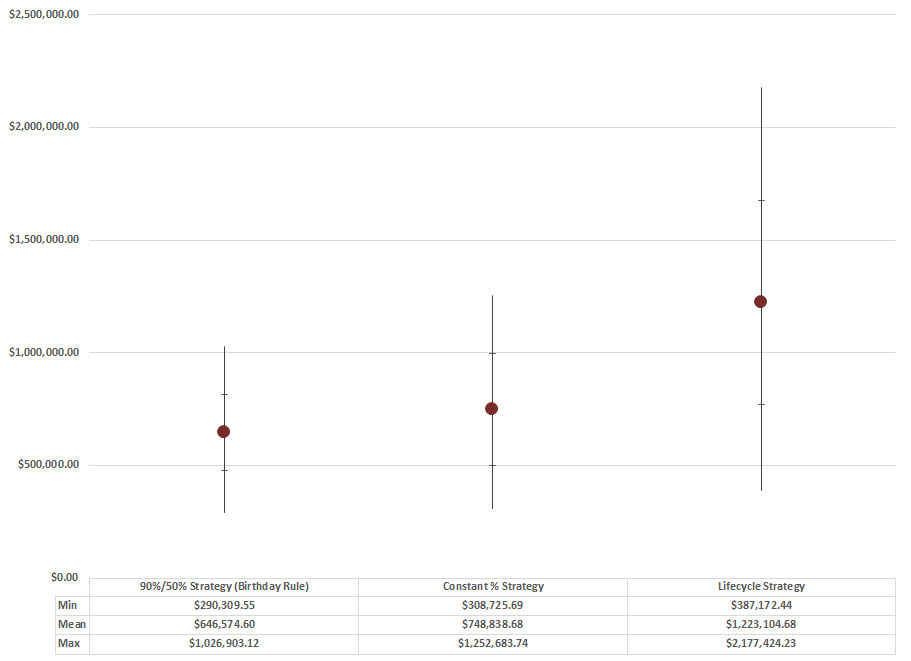

With the 200/83 lifecycle strategy, you'll end up with about 90% more compared to the birthday rule, and 63% more wealth compared to the constant strategy. Even the downsides are better - 33% and 25% more respectively. The strategy's risk (the standard deviation) is higher at 37.05% compared to 26.09% and 33.36%. Another way to measure this risk is with the Sharpe Ratio; it's used to evaluate the risk-adjusted performance of an investment. The birthday rule had a Sharpe ratio of 2.12, constant had 1.84, and lifecycle had 2.06. In other words, the constant portfolio is riskier than the lifecycle strategy and doesn't have the returns to show for it. The lifecycle strategy is slightly riskier than the birthday rule, but its expected return is much higher!

You may have heard the quote that claims "diversification is the only free lunch" in investing; that still stands, but this is pretty close. By following the lifecycle strategy and reducing your stock exposure at retirement to 50 from 83, your outcome is better for almost no additional risk! Both the 200/50 and birthday rule end up with the same 26% standard deviation.

The increased exposure is what boosts your returns, while the better allocation across time is what keeps the

risk under control.

Your Sharpe ratio also comes out ahead at 2.34 vs 2.12. This is a big deal because it attributes the outperformance to diversification as opposed to investing more money or taking additional risk.

Bear Gang

Markets don't always go up. When they don't, levered portfolios get hit harder. With this strategy, a market drop is even riskier because it pushes our leverage over 2:1 as equities get hit. The strategy requires the investor to maintain 2:1 in that initial decade which means buying more as prices fall.

Of all the 96 back-tested simulations, the 200/83 rule came out on top even during market downturns. Those entering retirement in a downturn aren't affected because they no longer have leverage, and the unlucky person in their 20s who just started may see a significant drop of a much smaller portfolio, which will recover over time.

This strategy is definitely not for everyone. Chapter 6 is one of the most important chapters as it cautions investors not to overdo it.

- 2:1 is the recommended maximum.

- High-interest debt should be dealt with beforehand. Don't go chasing an 8% return while paying 20%+ on credit cards.

- If your employer matches on a 401k plan, take that money! You'll get market returns + a risk-free contribution from your employer.

- Don't do this with your house's down payment or children's college money

- This isn't for people with jobs that are correlated with the market.

- This is absolutely not for those who can't take any risk. A good measure will be how often you check your brokerage app or refresh it when prices are in free fall. I recommend reevaluating your risk appetite if you won't get good sleep during downturns.

- Most importantly, this isn't investment advice. Everything you've read so far is for educational purposes only.

The Fallacy of Time Diversification (2021 Update)

There are a few critics of this idea. Most of them believe the research is falling for the fallacy of time diversification. It's the belief that risk declines the longer you invest — that given enough time, the good years will cancel out the bad years. This fallacy doesn't work because each year of stock market return is isolated. Flipping a coin and getting twenty heads in a row doesn't change the odds of the next flip. Though I recommend getting a new coin — someone might be cheating. The same idea applies to the stock market. Twenty years of good returns tell you absolutely nothing about year twenty-one. They are isolated, and investing longer does not reduce risk.

The lifecycle approach doesn't fall for it. The strategy doesn't reduce your risk because you're buying and holding stocks for a longer period of time. That's impossible to do. Any return above the risk-free rate is subject to capital loss as well as capital gain! Risk is double-sided. The longer you invest, the more bets you take. And by taking more bets, you increase your chances of making and losing more money. Say you start with $10,000 in year one. The total amount you can lose is $10,000. If the market returns 7%, by year 2, the total you can lose jumps to $10,700. But your expected gain also jumps because you have $700 more invested.

We've already established that money invested at a younger age is more impactful. It goes through more cycles and is exposed to more ups and downs. The lifecycle strategy suggests bringing forward some of the future income by using leverage. On the surface, and definitely in the short term, it looks riskier. But over a long period of time, you end up taking more evenly distributed bets. Most of that future income only gets released at an older age. By then, you would have missed many market cycles. The market returns and distributions are the same in both scenarios. But getting more cycles introduces the law of large numbers.

💻 You can run all these numbers yourself - download the dataset and simulations from the book's official website

📧 If you found it interesting, share it with people that could learn a thing or two

❤️ Subscribe here for future notes

📚 Currently Reading LinchPin