Lifecycle Investing - Invest Time For A Better Retirement Outcome

Fixed income may be suboptimal for young investors with time. Portfolio returns can be optimized by taking a holistic approach to planning.

Tolu Salako

Tolu Salako

Start Here

Investing can be intimidating for most people — it's a game you play with your hard-earned money. Even worse, you can't influence the game's outcome. As humans, we're wired to sell low and buy high because losing money hurts more compared to the feeling of making it. So, we come in playing defensively by default. We'll mix some bonds in our portfolio to reduce the pain if the market tanks, even if it means sacrificing substantial returns. For most, some returns are understandably not worth the risk, but that doesn't apply to everyone. Each individual has a different income, debt, savings, risk tolerance, and most importantly, goal in mind when they invest. So why do most follow the same general rule of thumb like a 60/40 target allocation?

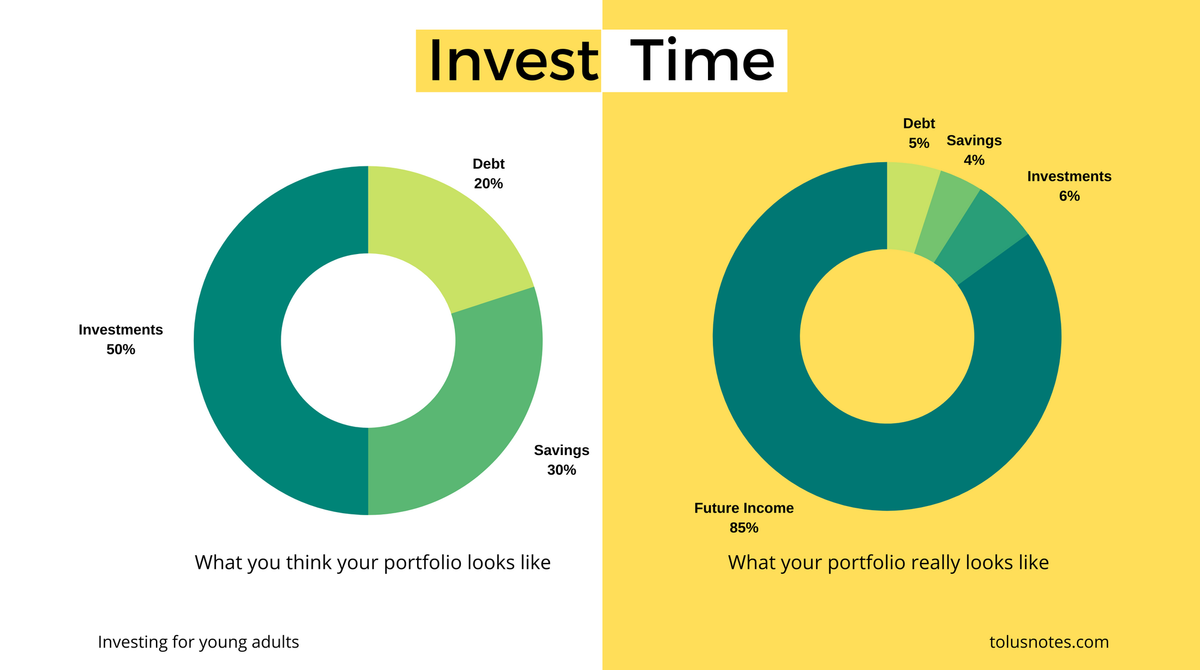

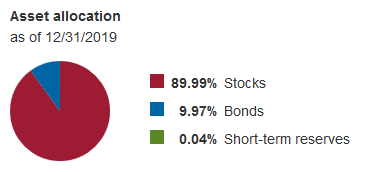

There's a reason things like the 100 rule and target-date funds exist. These funds allocate a percentage of your asset to stocks and the rest to fixed income. As you get older, your risk appetite reduces, and more stocks are replaced with fixed income. For me, a 24-year-old, my target-date fund will be a 2060 retirement fund, much like Vanguard's VTTSX. The current allocation has about 90% in stocks.

For starters, this works. I'll be okay in retirement if I stick to it. But a portfolio made up of this fund won't help me reach my financial goals, and it may not help you either, even if you're risk-averse. The main reason is that age isn't sufficient when determining asset allocation. It ignores the fact that most young adults are currently working and expect to continue working till retirement. We already have fixed income in the form of our current and future compensation for our job, and it's the largest part of our lifetime portfolio. You can view this part of your portfolio as your human capital.

You can’t time the market. But you can time yourself. You know how many years you have left till retirement and how much of your income you are likely to put aside during that time. You can use this self- knowledge to diversify your exposure to the market.

Ian Ayres & Barry J. Nalebuff - Lifecycle Investing

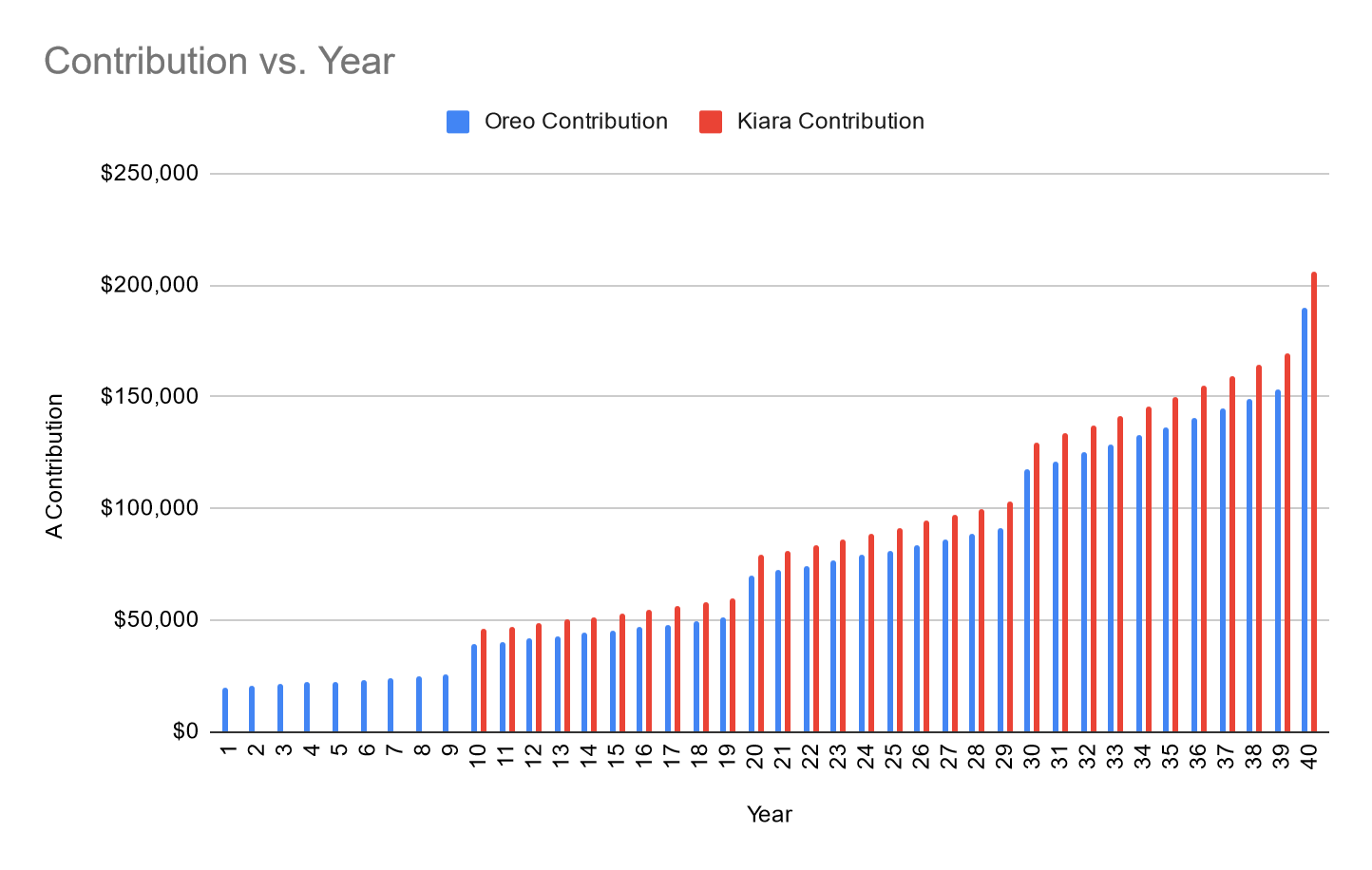

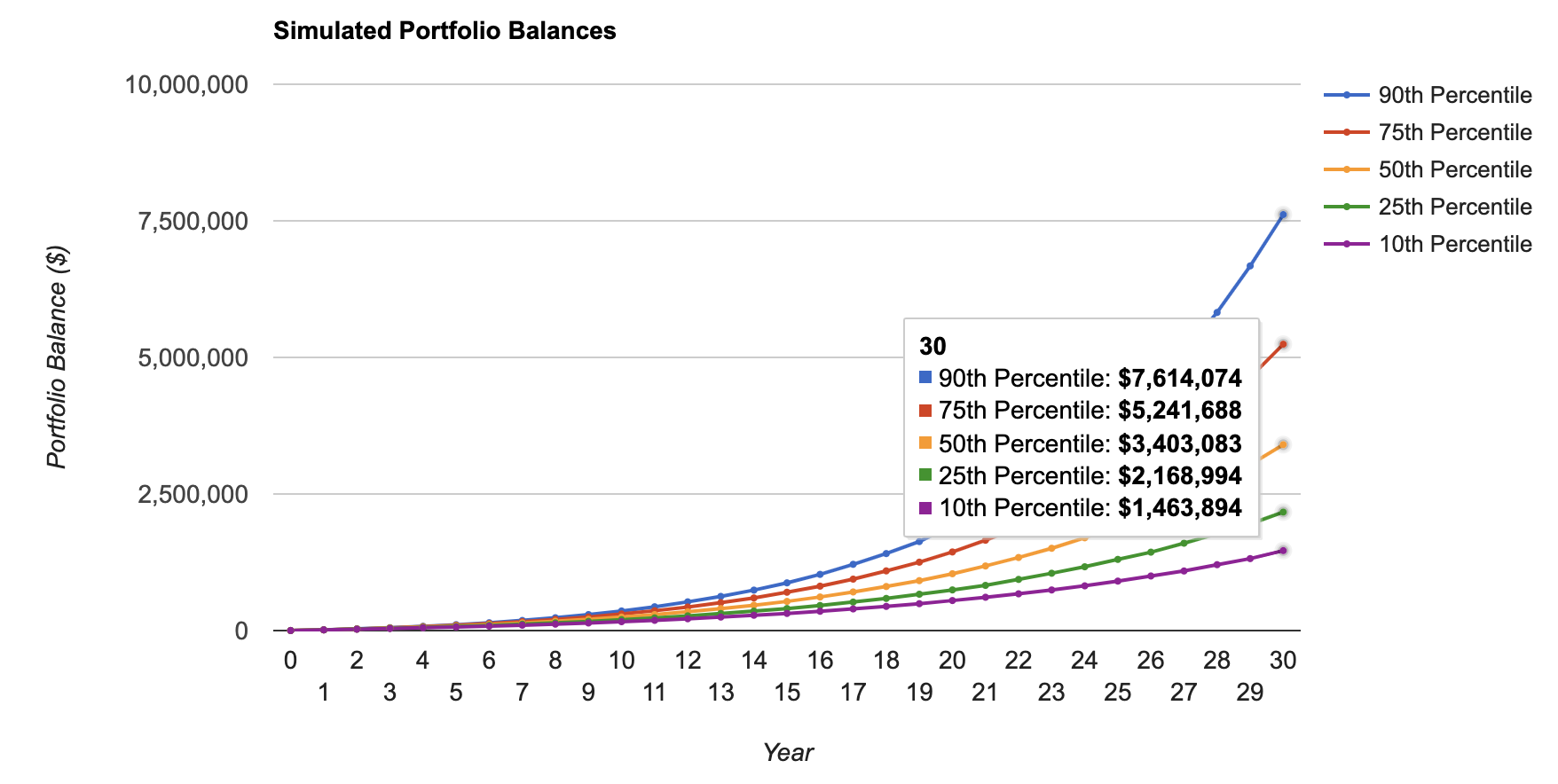

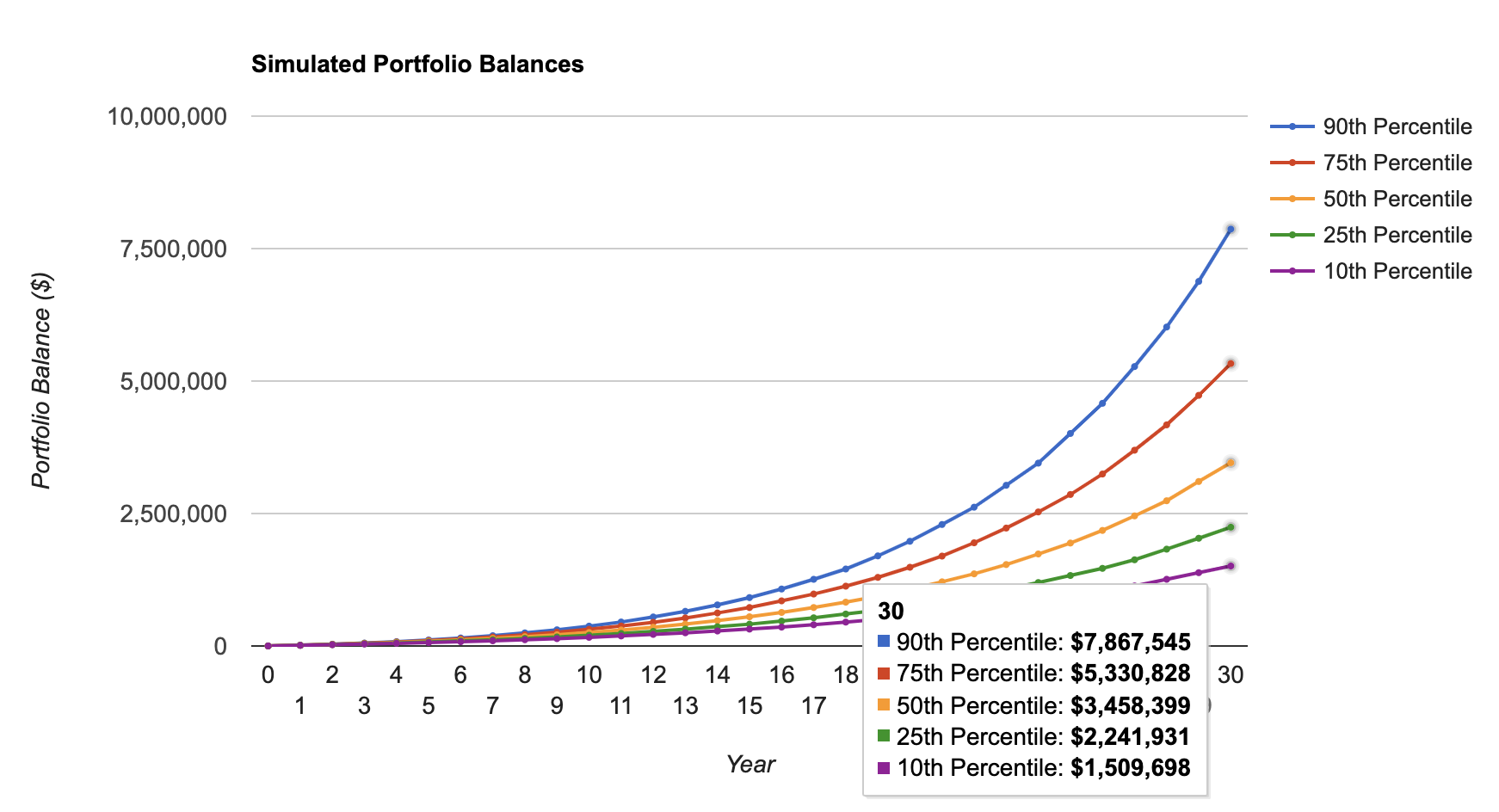

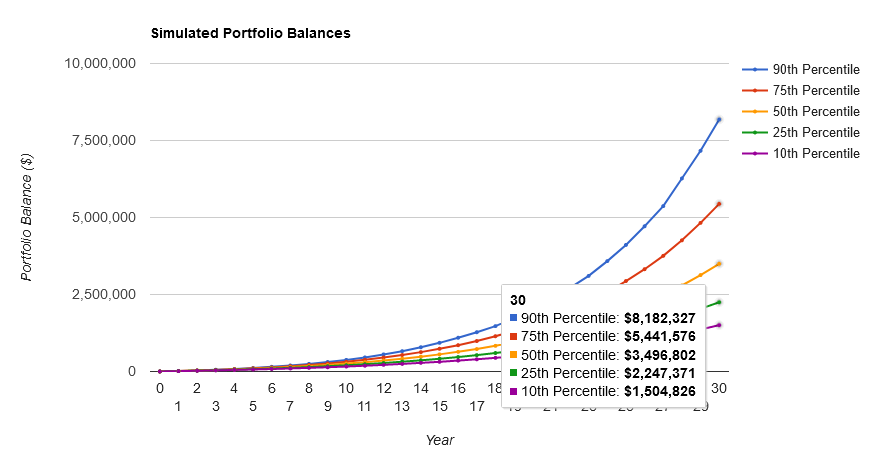

Lifecycle Investing is a brilliant book. Though I'm not recommending a 200% stock portfolio like they are, the concept of including your future income in your asset mix makes sense. Thinking holistically can end up reducing risk even with the additional exposure to stocks. Take a look at the following Monte Carlo simulation. All three investors start with $1000 and contribute $12000 per year to a 100% stock portfolio. The only difference is when and how much they invest at any given time. The first contributes a lump sum of $12,000 per year; the second divides it into $3000 per quarter and the third $1,000 per month.

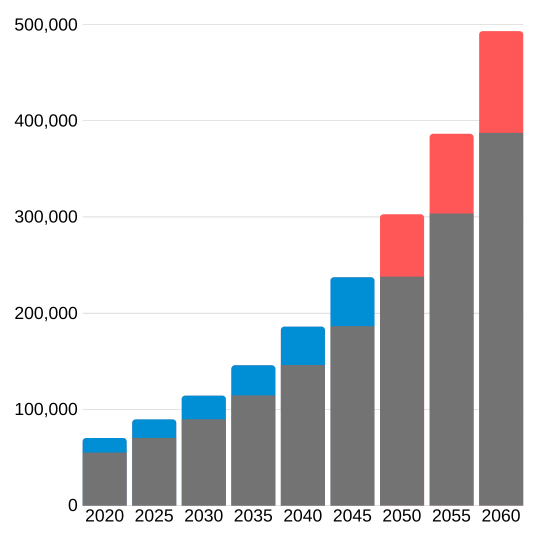

The 50th percentile (the most likely outcome) is better off for the investor that spreads out their contribution over an extended period of time. We know that diversifying reduces risk, but we only think of it in terms of assets (buying index funds vs. individual stocks). Most fail to diversify across time by limiting their market exposure to the later years of their lives. This isn't intentional. It's because we're making less than what we'll eventually make. Take the following, for example. You're currently making $70k per year and investing about $15k (20%) of it every year. Assuming you get a raise or new compensation increase of 5% per year and continue investing about 20% every year till you retire around 2060.

A majority of your contributions will happen in the final decade before retirement. This means that the expected outcome of 50% of your contributions is determined by the final decade. The other half had more than double the time, meaning it experienced more cycles and compounded more. That expected outcome is even less desirable because some of those contributions will go towards fixed income given the proximity to retirement.

The greatest way to optimize the positioning of a portfolio at a given point in time is through deciding what balance it should strike between aggressiveness and defensiveness.

Howard Marks - Mastering The Market Cycle

Dear investor, I'm writing this now because stocks are more expensive than usual. The higher the market is, the lower the expected return becomes. This applies to stocks as well as bonds. It isn't market timing; it's due to the inherent cyclic nature of the market. I'm not asking you to sell when you think the market is at the top and buy when you think we're at the lowest lows; no, that strategy would fail miserably. I'm asking you to reevaluate your asset mix with your future income in mind. You obviously don't know what this number is, but try to estimate it before allocating more fixed income in your portfolio.

This all depends on your risk tolerance. Ignore all of it if you have bonds in there to prevent you from selling during a downturn. Ignore it all if you need fixed income or have a smaller percentage of future income compared to your current net worth. Most importantly, ignore it if you pick stocks or are not properly diversified. But if you're a young adult with time and an appetite for a little more risk, you're better off diversifying across time! 100% in stocks now can dramatically increase your income at retirement. You only get to be in your 20s and 30s once!

📧 2/3rds - think of 3 people that could learn something from what you just read; send it to the first 2.

💬 Let me know what you think of this piece - reply to the newsletter or email me directly at newsletter-at-tolusnotes.com.

❤️ Want more? - subscribe here for future notes.

🏈 Go Niners - insight from a random name generator.