Growth Investors, Let Luck In

Those who believe that Big Tech can't fail are no different from those who believed in the superiority of the Nifty Fifty or Big Oil.

Despite the following intro, this note is related to the stock market.

When I was in the market for my first rental property, I had to learn a ton about real estate. This was after starting a company in the industry, and while working at a different one. I had one guiding principle: buy what makes sense financially. It eventually led to me spending a few months creating a spreadsheet model to do just that. Whenever an interesting property came up on my MLS alert, I'd plug in the address and listing price, and it'd tell me if buying made sense. If it didn't, I didn't even bother looking at the property images. My search, which started in the bay area, did not end there because the model denied everything I threw at it.

Unlike real estate, stock market returns can't be easily modeled. Both have expected and unexpected returns, but the stock market's liquidity makes things more difficult. If you were to check your portfolio on a particularly bad day, you may be more inclined to click SELL instead of BUY. That's not necessarily wrong. After all, that's how you feel, and it is your money. But imagine checking your Zestimate on a bad day. You're less likely to consider selling. Even if you did, your mood would be different by the time a real estate agent gets back to you. You're still stuck with the property until you sell it months later (assuming you're not using an iBuyer like Opendoor). The same thing goes on the buy-side.

This lack of liquidity, among other things, acts as a barrier that forces investors to give more thought to transacting. The lack thereof in the stock market gives investors unlimited freedom to transact as many times on as many whims as they can. And thus, we're never truly at an equilibrium. Human investors and their human-controlled counterparts have evolved to either be too greedy or too fearful. We expect good things to continue endlessly, and think the world is about to end whenever bad things happen. It's just how we are.

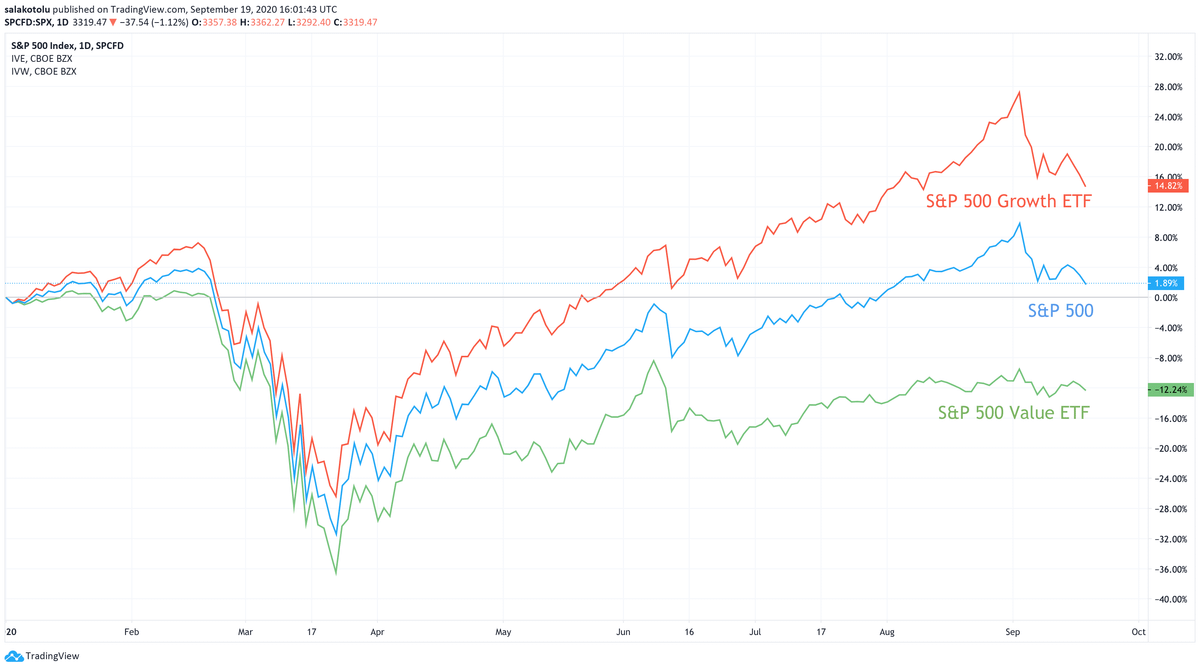

This year, investors have shifted a lot of money from value to growth. Large-cap growth companies in the S&P 500 have returned 27% more than the value companies in the index. This isn't atypical considering how the pandemic may have strengthened these companies. Netflix and Amazon obviously benefit directly from social distancing and lockdowns. Investors that realized it in March made a killing, but it didn't stop there. Investors pushed growth companies to new levels. If these companies continue to meet and blow past expectations, then great. But it won't be enough. Growth companies would need to continue raising the bar. This feat, while not impossible, is very unlikely.

Historically, the S&P 500 has returned anywhere between 8% and 10% on average. This is the standard. Investors choose to risk their money because they expect to earn a premium. Anything higher is unexpected. When prices are high, the expected returns are lower. Right now, the expected returns of large growth companies are very small. Look at it this way. If you bought a stock that returned 50% in a month, would you expect another 50% the next month? No. You'd count yourself lucky and frame a picture. Large growth companies have exceeded expectations even from their depressed levels.

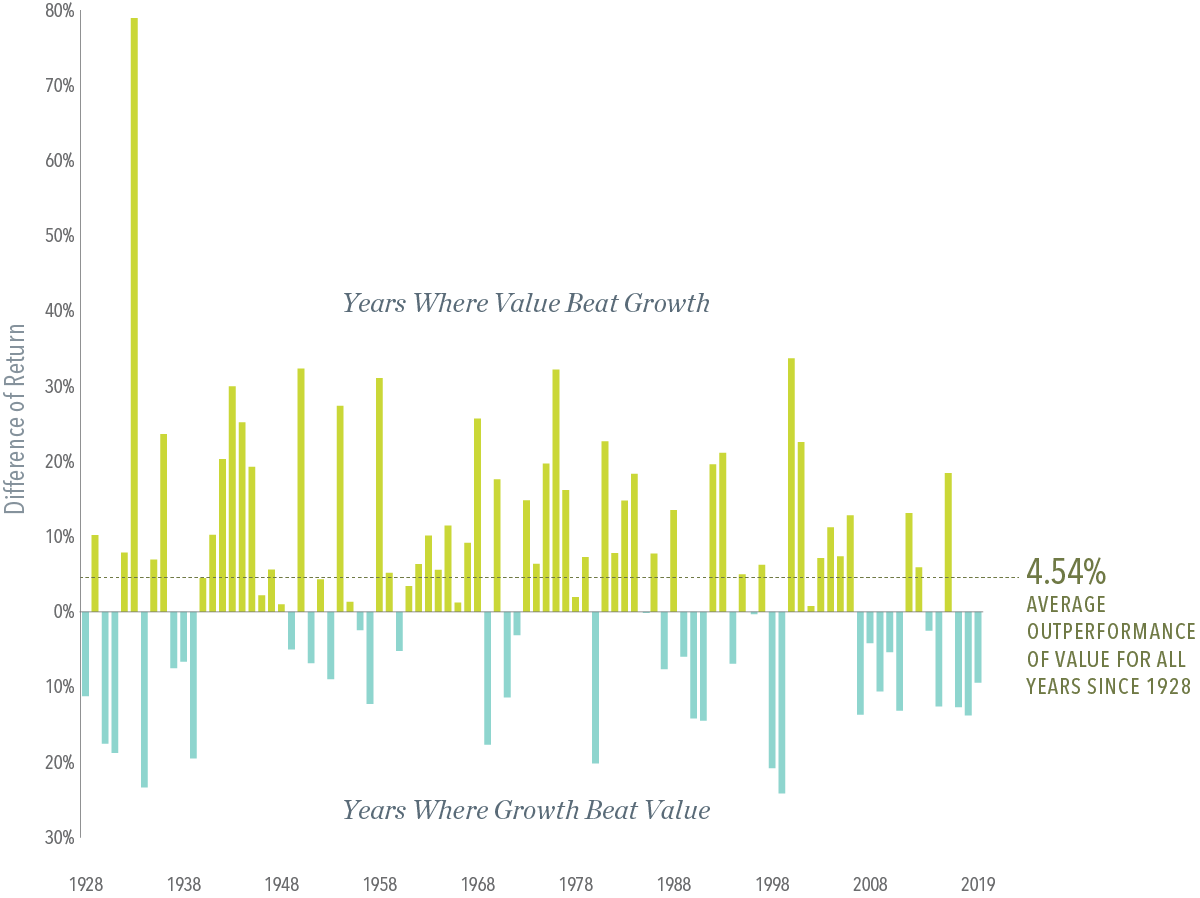

Growth companies may warrant certain hype, but they usually fall out of favor for more reasonably priced companies. In the last decade, growth stocks have left value in the dust largely thanks to FANGAM. It is not uncommon for a few stocks to carry the entire index, but it is unlikely that Amazon, Apple, and Netflix will see quadruple-digit total returns in the next 10 years. Though they are the innovators of our generation, they'll likely become stories for the future. IBM, AT&T, Exxon, GM, and GE were all innovators during their time. They were some of the top 10 U.S. large companies. Though some remained at the top for decades, they underperformed the market after making the top 10 list.

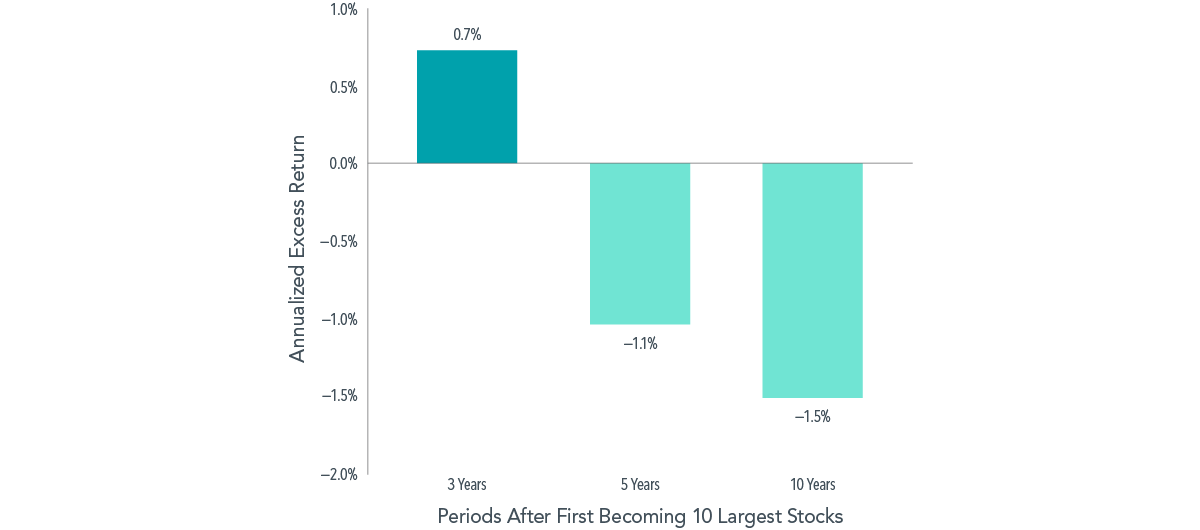

Dimensional Funds looked at large U.S. stocks after making the top 10 list (by size) from 1927-2019. They noticed that those companies continue to outperform in the short-term, but fail to beat the market in the long run. You could argue that things are different now, that no price is too much for innovation. You could also argue that past performance doesn't guarantee future results. But that'll be the exact point I'm trying to make. Netflix, for example, returned 3,726.2% in the last decade. I'm willing to bet that this decade will be lackluster in comparison.

Those who believe that Big Tech can't fail are no different from those who believed in the superiority of the Nifty Fifty or Big Oil. No? It's different this time? Sure it is.

This is not a warning to dump all large-cap growth stocks. I know just as much as you do and have no idea what the future holds. Large-cap growth stocks can continue to have crazy returns. The idea is not to get rid of them, but to include small and value stocks in the mix. Unlike the S&P 500, Total market ETFs like Vanguard's VTI provides exposure to the entire market. I'm personally heavy on SPY in my taxable accounts, so I tilt my retirement portfolios towards small value. The point is to capture the entire market.

The recent underperformance of small value stocks is also great for young investors. It provides the opportunity to accumulate more given current valuations. If you believe that the market is cyclical and that we'll see investors rotate back to favoring value, then it's best to position your portfolio in order to get lucky. This isn't guaranteed, however. Nothing is.

I discussed some of the topics in today's notes in my conversation with Casey Burns. It's around the 15 minute mark.

If you have time, I also recommend checking out Ben Felix's video which released while I was editing my draft. His channel, along with their podcast (Rational Reminder), are priceless resources for those playing the long game. They are the experts on this stuff.

Sources

https://www.dimensional.com/us-en/insights/large-and-in-charge-giant-firms-atop-market-is-nothing-new

https://www.dimensional.com/us-en/insights/when-its-value-versus-growth-history-is-on-values-side

Launched a podcast this month. Listen & subscribe wherever you get your podcasts. The next episode will feature an early subscriber (first 30), and we'll discuss everything from private capital to crypto currencies. Stay tuned.

Spotify | Apple Podcasts | Google Podcasts | RSS

✉️ Thanks for reading. Let me know what you think of it at newsletter@tolusnotes.com

❤️ If you enjoyed it, please forward it to support the newsletter.

👊 If this was forwarded to you, you can subscribe here for future notes

📚 Currently reading Outliers: The Story of Success

Tolusnotes participates in Amazon Services LLC Associates Program. We earn a small revenue from qualifying purchases.