What Value is Wealthfront Providing?

It's time to re-evaluate what you're paying for.

Wealthfront is a robo-advisor that offers several financial services. They're mostly known for their investing platform, but they also have a savings account, and a portfolio line of credit. This post will focus on critiquing their investing related services.

Tax-loss Selling

Whenever I sit down to explain why Wealthfront isn't worth it, tax-loss selling / harvesting is one of the biggest reasons people use their service. Simply put, you can sell positions for a loss and write it off during tax season. There are rules as to how long you have to wait before buying back in, or what you can buy back immediately, but the point is to save you money on taxes. Wealthfront automates this event for you. Contrary to what their page says, tax loss harvesting is only available for taxable accounts. Seems obvious, but I know a few people who pay specifically for this service, but don't have a taxable account with them. Selling a stock in retirement accounts like a 401k or IRA won't trigger a tax event. You don't owe taxes till you withdraw money from that account. Their invest page claiming that tax-loss harvesting is "available for all investment accounts" is misleading.

Risk Parity

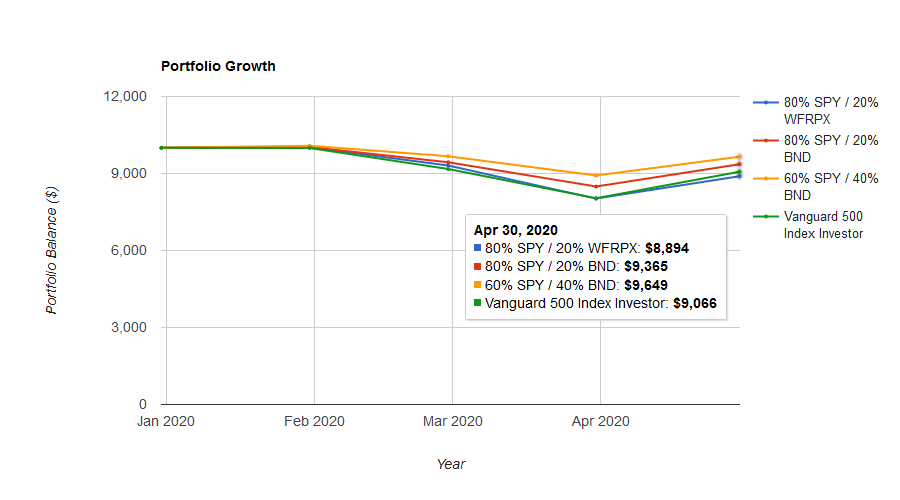

Sometimes market returns are not good enough. Most investors, myself included, aim to beat the market. My approach is to strategically lever up with options, taking more risk for a chance at netting higher returns. Wealthfront's approach is a bit different. Their risk parity fund aims to increase risk adjusted returns by allocating a percentage of a portfolio to other asset classes that tend to do well when stocks aren't too flashy. The fund is still too young to draw any conclusions, but it did not perform as expected when the rona hit us. Let's take two portfolios for example. Portfolio 1 is made up of 80% SPY, and 20% WFRPX (their risk parity fund), and portfolio 2 replaces their fund with BND (Vanguard Total Bond Market ETF). I'm allocating 20% to their risk parity fund because that was their default allocation when they automatically enrolled qualifying members after the fund launched on January 2018.

If you invested $10k in each fund at the beginning of the year, you'd be down YTD with $8.9k in portfolio 1 (includes risk parity), and $9.4k in portfolio 2. A simple 60/40 portfolio would have been better.

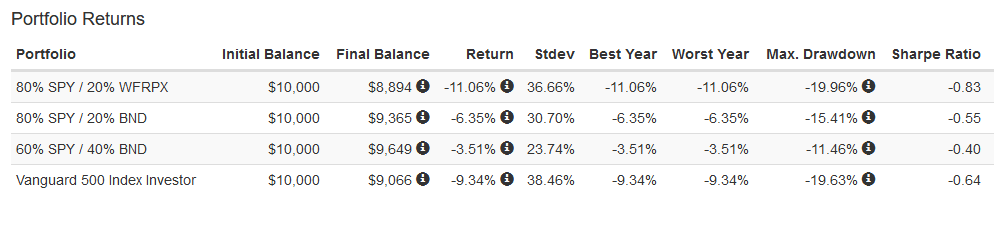

Even worse, the portfolio with the fund has a sharpe ratio of -0.83 during this period, much lower than -0.64 in an all equity portfolio invested in the S&P 500. This means that investors don't have the returns to show for the amount of risk they are taking, or trying to avoid in this case. While it's too early to judge this performance, a black swan event / downturn like the rona is exactly what the fund was designed to protect against. Having a lower risk adjusted return is not a good sign, especially when investors are paying an additional 0.25% on the capital invested in this fund in addition to the 0.25% advisory fee. Don't reward under-performance, read TN03.

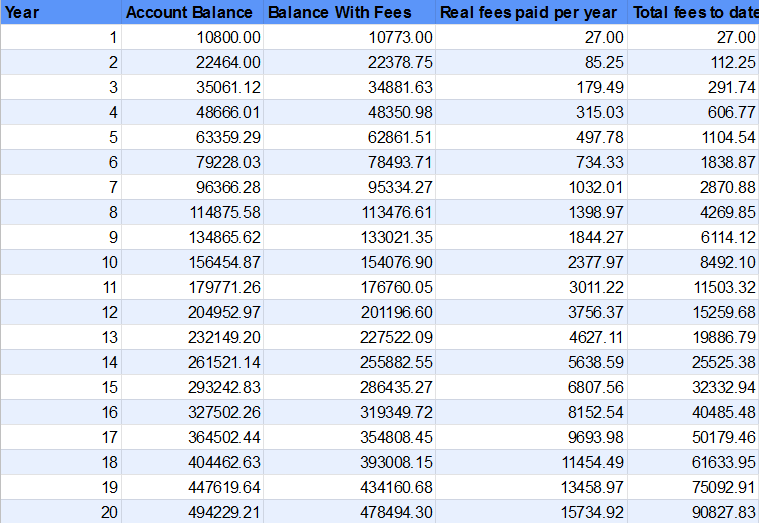

Fees

A $10k portfolio with 20% allocated to the risk parity fund will pay $30 bucks a year. $5 ($2k * 0.25%) plus $25 ($10k * 0.25%). This seems fairly small, but this isn't the right way to do the calculation. Let's simplify it a bit and assume the $10k portfolio isn't invested in the fund, so it's just paying 0.25% per year. Let's also assume that $10k is added per year, and the portfolio gains 8% annually. After 20 years, the Wealthfront investor would have paid over $90k in real fees if we take opportunity cost into account. The image below tries to show what the portfolio would look like if it never paid those fees, and if that capital was put to work instead.

$90k is 45% of the investor's $200k contribution over 20 years. The Wealthfront investor in our example would have paid almost 20% of their final portfolio balance in real fees (90827/478494) by year 20. Compound interest works both ways. Make sure you know exactly what you're paying for.

Smart Beta

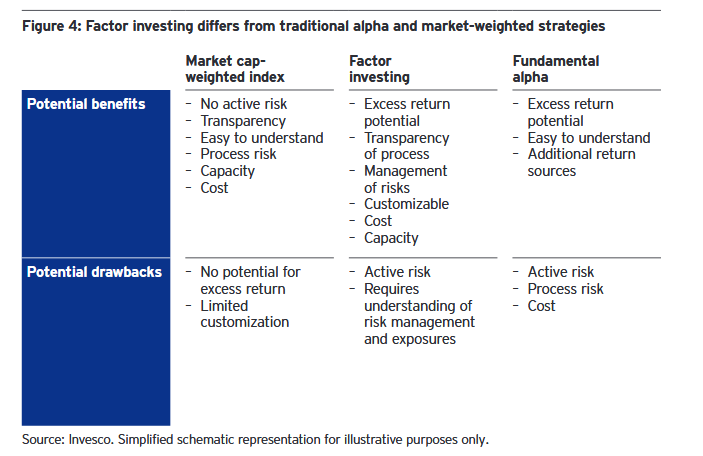

Investors with over $500k in their taxable account can enable Smart Beta - an investing strategy that aims to increase expected return by weighing stocks based on factors instead of market cap. For example, the S&P 500 ranks companies by market cap then allocates funds to those companies based on how big they are. A factor tilted portfolio does not blindly trust a company simply because it is large. Instead, it weigh stocks (and ETFs) based on size, value, momentum, quality, minimum volatility, and dividend yield. This is probably the only service they offer that's worth paying for, but chasing excess returns comes with its own risks.

The risks it introduces are different from what we normally discuss. If we shift our portfolio away from bonds, and add more stocks, we are increasing risk by increasing our exposure to equities. Tilting a portfolio towards one or more factors won't necessarily increase that same exposure or risk. However, it introduces the risk of active management or tracking error.

Portfolio Lock In

If you decide to leave Wealthfront, you can simply transfer your account over to another brokerage. If your account holds VOO, you'll get VOO in the new brokerage unless you enabled their Stock-level Tax-Loss Harvesting. In this case, you'll still get VOO, but it'll be in the form of 500+ individual holdings instead of a single ETF. Direct indexing helps them save you more on taxes, but it also keeps you on their platform till you decide to do something about it.

Alternatives

Unless you're taking advantage of their tax loss harvesting (in a taxable account), you'll save thousands by going with a free brokerage. Wealthfront may also be for you if you really believe in their implementation of Smart Beta and Risk Parity. To an extent, Wealthfront is no longer a truly passive investing platform. It's why they call it PassivePlus®.

Personally, I use M1 finance along with TD Ameritrade for options. With M1, I can automate my contributions, capital allocation, rebalance automatically or manually, and borrow against my portfolio without paying any transaction or management fees.

Why pay someone else when I can under-perform the market all by myself?

😧 Did you know that this section is different each time? A subscriber assumed it was always static

✉️ Are you sticking to Wealthfront? Let me know why at newsletter@tolusnotes.com

❤️ If this was forwarded to you, you can subscribe here for future notes

📚 It's About Damn Time by Arlan Hamilton & An Economist Walks into a Brothel by Allison Schrager

🎈 Turned 25 on Wednesday. Life is cool!

Tolusnotes participates in Amazon Services LLC Associates Program. We earn a small revenue from qualifying purchases.