Volatility, Uncertainty, and Finding Clarity

This time, it's not different

What a year it's been. First, the U.S. assassinated Qasem Soleimani, then the Coronavirus Disease became rampant, and now the country is deciding to have an election - in 2020 to say the least. Jokes aside, we knew about the election, but we didn't know about the airstrike or the virus; there was no way we could have prepared for them. As investors, we view the price of a stock as an agreement, a consensus, that the company is worth X because it has Y assets that will be worth Y + Y2 in the future, and has sold Z things and is expected to sell Z + Z2 in the future (give or take). That price will move slightly from day to day as more information becomes available or due to pure speculation. But most of all, the price reflects what people are thinking – shorts agree it should be lower, and longs think it should be higher. But when investors suddenly change their minds, volatility is born.

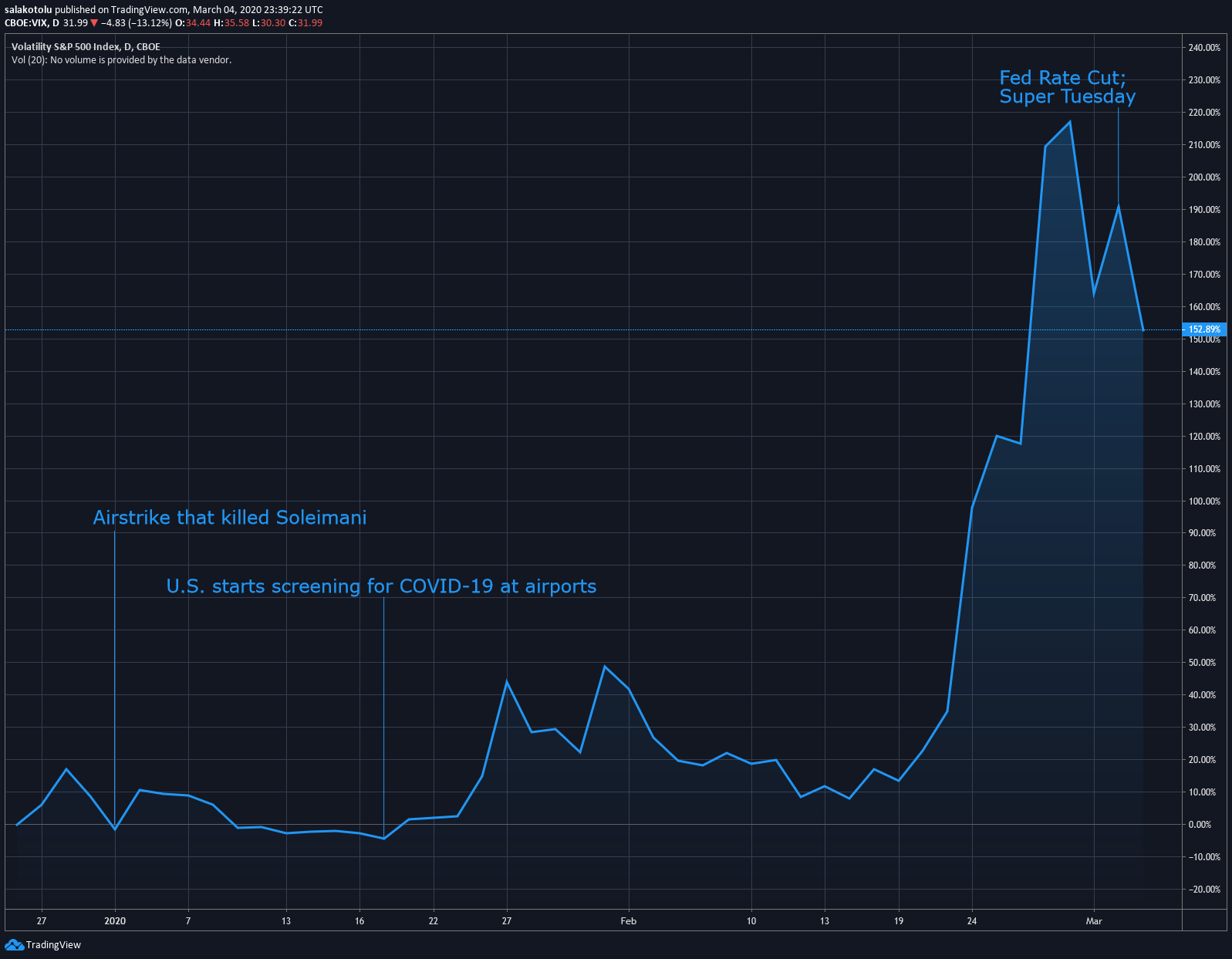

Most investors weren't expecting the U.S. to kill an Iranian general, but the event didn't create any uncertainty. The virus, on the other hand, directly impacts the second largest economy in the world, including cascading effects caused by disruptions in the supply chain of many American companies. And yet - no effect; investors remained certain that everything would be fine. That was until the virus took a first class seat across U.S. borders to pay Americans a visit, then panic ensued. This was no longer just about returns as investors began to worry about their health and safety. Black swan-like events like the virus (it isn't a real black swan) carry a lot of uncertainty that confuses investors and forces them to renegotiate previous agreements. This sudden reaction to uncertainty increases volatility as investors try to make sense of the virus.

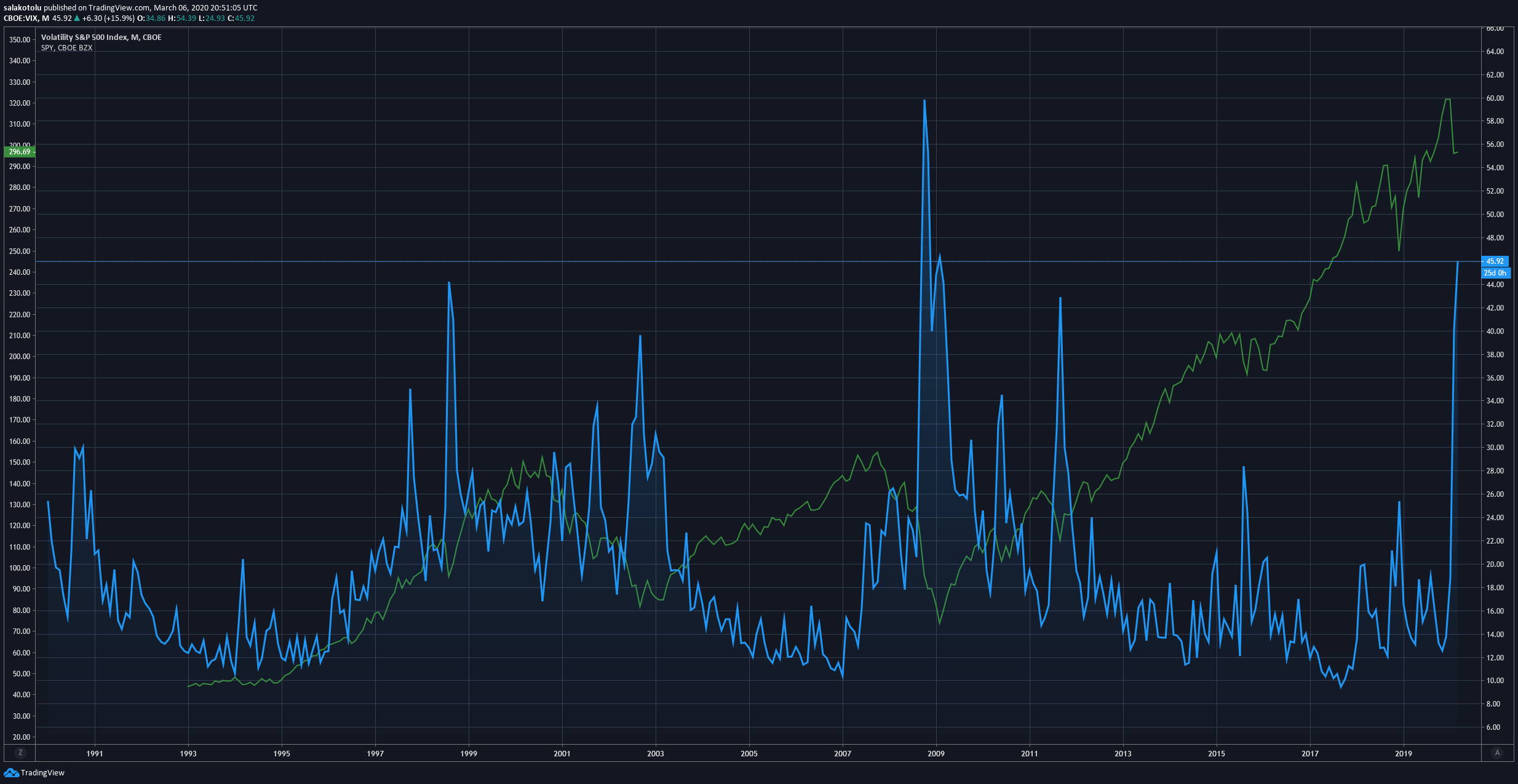

As of Friday, the volatility index, also known as the fear index is accelerating towards 2008 levels. The market hasn't crashed yet, and though sustained levels of uncertainty can make that happen, it is unlikely. But that's just speculation, no one really knows. What I do know is that volatility is very high, and the virus is the root cause (there are other factors at play, but this is the main one).

Back to Basics

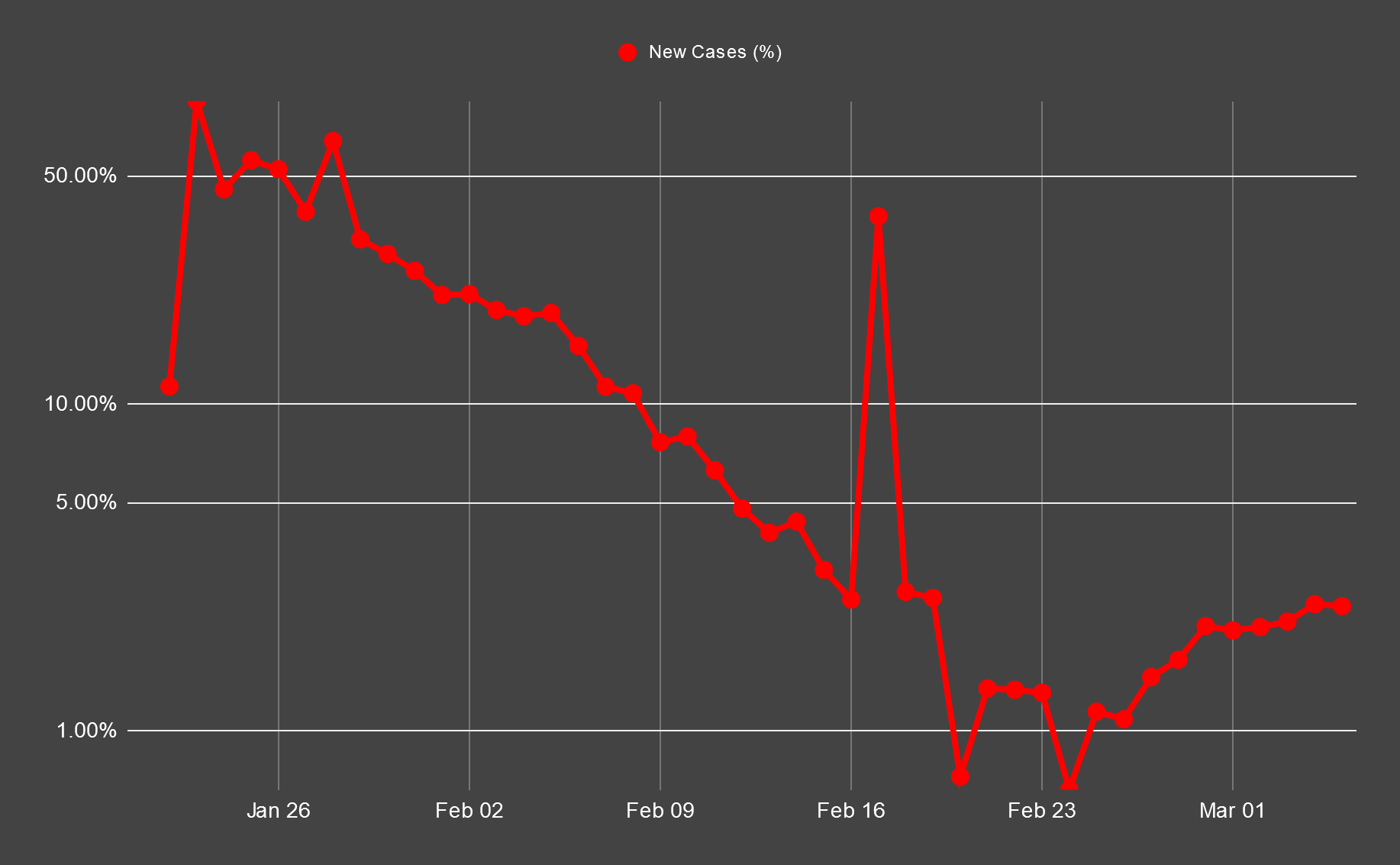

At this point, any news other than a reduction in new cases or a vaccine is bad news. Even no news is bad news and the market may continue to react the same way it has for the past few weeks. The virus isn't slowing down; it could continue to drive prices even lower. But there is always an end no matter how uncertain the future looks. We won't live in fear of the virus forever. Even if it's never contained, it'll lose it's novelty and life will resume as usual. In fact, the news will be the first to lose interest and move on to the next interesting topic. The virus will vanish from our minds, but it'll leave a trace on the economy – companies will obviously report reduced earnings as a result of the temporary disruption. This is known; it has been priced into current valuations. Our job as investors is sifting out the noise in search of the truth, in search of clarity. No one knows what the future holds, but we can call on history to help us get a better sense of what to expect.

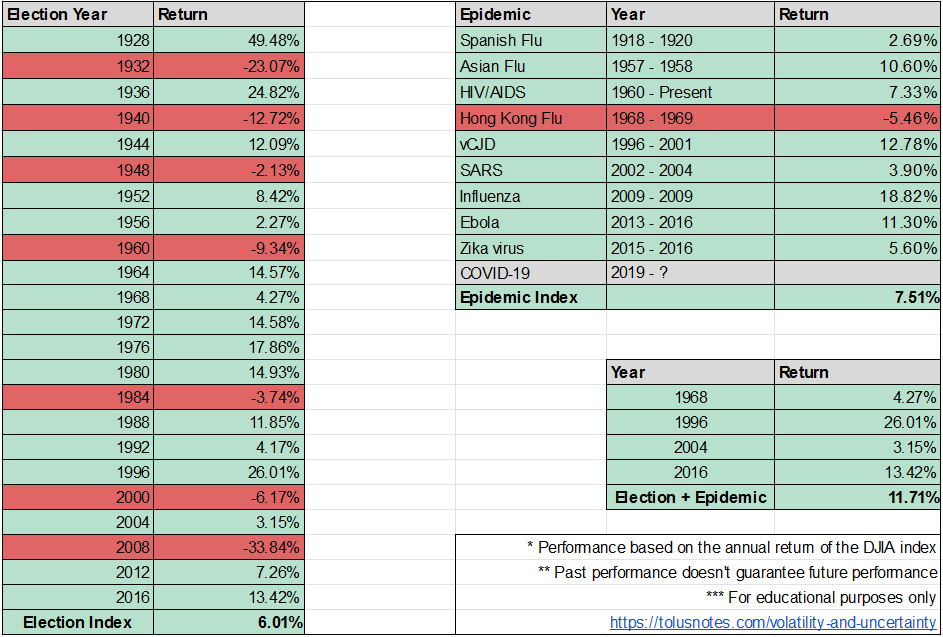

The most uncertain events plaguing the market are the 2020 elections and the Coronavirus. Using historical annual returns of the Dow Jones Industrial Average, I created some hypothetical indices that tracked returns during years with an election or an epidemic crisis. Historically, from 1928 to 2016, investing during U.S. presidential elections returned 6% on average – you made money 70% of the time. That return improves to 11.3% if the S&P 500 index is used, but I'm sticking with the DJIA because it goes all the way back to 1915 vs. the S&P's 1928. The same goes for epidemics. Investing during worldwide epidemics returned 7.5% on average. We also have a few data points on years with both an election and an epidemic. 1968, 1996, 2004, and 2016 all resulted in positive returns. Though this says nothing about the future, it tells us that investors who panicked and sold missed out during those years. It's easy to live in the moment and think that it's different this time – it's not. Even if we have a recession this year, we'll bounce back eventually. All you have to do is to stay invested.

Recommended Reading

- Nobody Knows II - Howard Marks

- Global Viral Outbreaks Like Coronavirus, Once Rare, Will Become More Common - Jon Hilsenrath

- Thinking In Bets - Annie Duke

💻 Cover image is from John Hopkins COVID-19 dashboard

📧 If you found it interesting, share it with people that could learn a thing or two

❤️ Subscribe here for future notes

📚 Finished Reading The Quants

Tolusnotes participates in Amazon Services LLC Associates Program. We earn a small revenue from qualifying purchases.