DeFi: Finance ReImagined For The Internet (FinTech x DeFi – Part 2)

With an infrastructure built from the ground up to address existing and potential issues, DeFi is an emerging paradigm changing the meaning of finance.

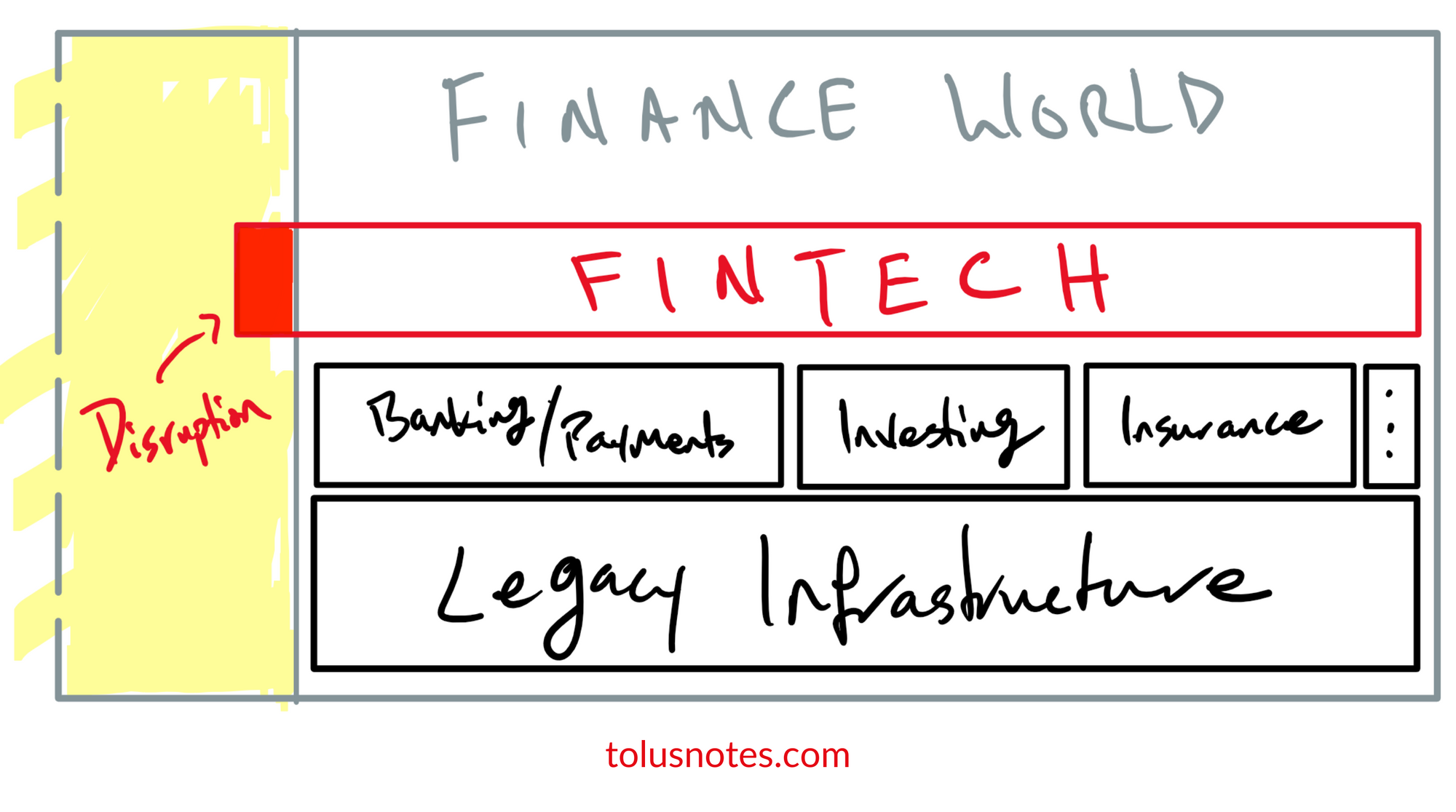

I initially titled part one "Where FinTech Failed." I updated it upon realizing that what seemed like a failure to disrupt finance stemmed from technology built on top of broken systems. Compared to old finance, fintech solutions look and feel new. User interfaces are sleek and straightforward. API designs now prioritize developers instead of salespeople. Overall, the user experience is just better. These are all welcome changes. The problem is that those upgrades are surface-level only. Fintech services look and feel new, but they are rough at their core. Feature-wise, fintech does not offer anything mind-blowing. Many fintech companies take traditional finance and slap mobile and internet on top of it.

Getting a mortgage is now an online native experience, thanks to services like Quicken Loans and Better. But instead of gathering and submitting tons of physical documents, you gather and submit tons of electronic documents. The countless back and forth between you and your mortgage expert has stayed the same. The back and forth between your mortgage expert and their underwriting team is still the same. The overall process still takes over a month, but at least it is online, right?

I spent most of part one highlighting the issues with online banks, but I have one more. As highlighted in part one, neobanks apply makeup to small traditional banks. It means, besides the nicer UIs, what you're getting is a small conventional bank. You can't instantly pay your friends with a neobank account unless they use the same neobank. That's not very different from what big banks have. Big banks are even better at payments because they have Zelle. Though the U.S. has a real-time payments network, big banks are not incentivized to pilot it for p2p payments because they already have an option. Neobanks, on the other hand, haven't rolled out anything of such despite not participating in a payment network like Zelle. Payment apps like Cash App and Venmo are cool, but fragmented account balances are not. The lack of low-cost instant liquidity is not.

Then there's investing — Part one highlighted some of the good things Robinhood has done for the industry, but let's not forgot the bad ones. Even with Robinhood, investing remains broken. I have multiple investment accounts, some long-term and others short. Sometimes those short-term moves turn out great. As any WSBer would do, I transfer those shares to my long-term account at a different institution. The good news is that all I have to do is upload the latest statement and specify what tickers and how much I want to transfer. The bad news is that it takes days.

The experience is still better compared to rolling over old 401k accounts. When I went through the process a couple of years ago, Fidelity sent me a check. I haven't worked for long, so it wasn't a huge check. But imagine getting a check that represents your decade-long savings and having to manually forward it in 2021? Switching costs should not be this high. Fintech investing solutions don't make it any easier to switch brokerages.

And then there is access to risk. Retail investors don't invest in the same markets as institutional investors. The same thing goes for accredited vs. non-accredited investors. Regulators decide where some groups can and cannot invest. Most unique wealth-building tools are locked behind wealth. The retail vs. institutional discord is ridiculous and unnecessarily polarizing, but people are onto something.

The makeup is starting to smear, and the cracks in the system are beginning to surface. Fintech is now maturing and, apart from a few exceptions, we have cool tech built on top of a crumbling infrastructure. The problems that need to be solved are at the core of the system, not the surface. I realize that some parts of these problems are regulatory, but technology should challenge regulation. Systems that improve productivity (labor or capital) should force us to rewrite the rules, not the other way around.

Fintech is finally bulky enough to start flexing. With mature businesses, it can begin focusing on infrastructure that it can leverage to offer more services. It can start challenging the status quo. Maturity will be good for consumers because technology can, and should, level the playing field. But while fintech companies weave their way around that, there's an emerging unregulated financial paradigm that's already running laps around traditional centralized finance.

Tolu Salako

Tolu Salako

DeFi

Decentralized finance is a new paradigm. DeFi is finance powered by cryptocurrencies and smart contracts. If you've managed to ignore crypto till now, start paying attention. "Crypto" has become a catch-all term for a number of things (similar to the term "machine learning"). Crypto is the volatile alternative asset that is bitcoin. It is also the stable USD-backed USDC. Indeed, the technology allows you to buy NFTs of digital horses, breed them, and race them. But it also powers many of the most disruptive and open financial systems that exist today.

A16z recently announced its third crypto fund [1]. Many of the mainstream news articles that picked it up only discussed the price and volatility of bitcoin. That's what crypto means to many people, so it makes sense that news sites will write what gets the most eyeballs. But no, a16z isn't spending $2.2 billion on bitcoin. That money is going to fund technology that even fintech struggles to keep up with today. And tomorrow, it may become mainstream. I think it will, but that's like part 30. We're barely on 2.

We're witnessing in DeFi what we should have seen in fintech if they had expanded beyond legacy infrastructure and regulatory boundaries. The infrastructure that powers DeFi has been completely reimagined and rebuilt from the ground up. Projects don't face the same bottlenecks they'll otherwise encounter in CeFi. Better yet, they get a leg up because the infrastructure itself handles many of the boilerplate work many centralized finance projects have to deal with (I will dive into these in a different piece).

DeFi isn't regulated yet. It's a wild west, but it is a beautiful mess. When there are no regulations, everyone tries everything — and I mean EVERYTHING — to see what works. Projects launch and projects fail, but most importantly, thinkers and builders keep iterating. The lack of regulation combined with continuous iteration is a good formula, but the nature and principles of the blockchain make it even better. Smart contracts, the tech behind DeFi, are open and trustless. It means you build your relationship with software, not with people or corporations. Due to this, projects are built in public. Code repositories are open source, and while that's nice, it's the community around these projects that keeps it going.

I played around with some DeFi protocols in 2020 but didn't dive in till this year. My red pill moment was when Archegos blew up. I kept wondering how one "small" family office could deploy so much leverage. Aren't regulators in place to prevent things like that from happening? Digging deeper, I realized that Bill Hwang "followed" the rules but got unlucky. He wasn't required to disclose anything because he didn't have much to disclose. But thanks to swaps, he had over a $100b position spread over multiple prime brokers incentivized to remain quiet.

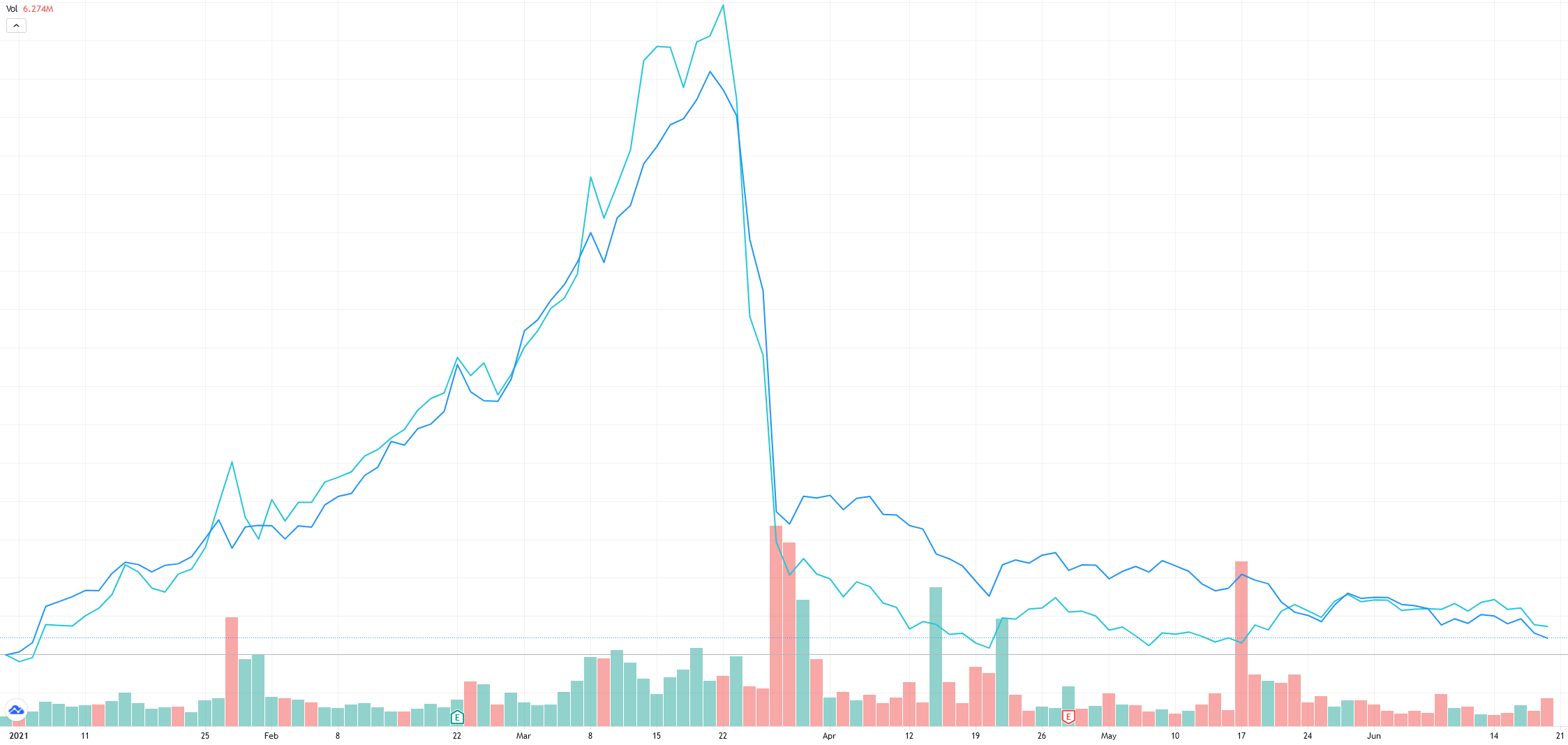

The chart looks a lot like two shitcoins (that's the term) getting pumped before crashing. It happens pretty often in crypto, mainly due to the lack of regulation and the abundance of speculators. But that is not a crypto chart. The chart represents the year-to-date returns of publically traded U.S. media companies ViacomCBS Inc and Discovery, Inc. The sudden rise and fall of these companies, among others, was thanks to Bill Hwang's leverage. Reports indicated that Archegos owned about $20 billion worth of Viacom by mid-march when the stock was trading around $100 [2]. Today, it's trading at $40 with a market cap of $26 billion.

Archegos made deals in private that affected every public shareholder, and no one except the prime brokers knew what was going on behind the scenes. At the end of the debacle, exact information on the size and reach of his positions is still hard to find. Other small family offices are likely doing the same thing but haven't been as unlucky as Hwang, and prime brokers would've continued lending to Hwang had Viacom not raised money. Let's compare this scenario to something else that blew up recently — this time in DeFi.

Terms are loosely deployed in the world of DeFi. Fully collateralized tokens like USDC (100% backed by USD) and DAI (150% collateralized by ETH) are called stablecoins. Uncollateralized tokens can also call themselves stablecoins. Very recently, I learned about iron finance over dinner with a friend. He claimed the protocol had an attractive yield. But to my surprise, iron finance was in a world of its own. I looked them up when I got home and took the following screenshot.

Iron finance blew up days after I took the screenshot. Their uncollateralized algorithmic "stablecoin" implementation failed due to a large-scale bank run. They addressed it in a postmortem on Medium [3]. People, including Mark Cuban, lost some money. But how cool is it that there was a postmortem? I'm sure we'll see some regulatory review of the Archegos debacle, but what if prime brokers were the ones leading the effort? It can't happen because of how incentives are structured. They couldn't even coordinate amongst themselves.

#DeFi problems are technical issues that will be fixed in time with incentives.

— Tolu 📝 (@tolusnotes) June 15, 2021

TradFi problems are structural issues that are difficult to fix due to incentives.

Leverage is no stranger in crypto. Centralized exchanges (CEX) like Binance let traders lever up to 100x (it's much lower in DeFi). Some of that 100x leverage heavily influenced Bitcoin's runup. When prices dropped in May, people knew what to expect because they sensed how much leverage was in the system. Even better, people grabbed some popcorn as they watched overly levered accounts get liquidated in real-time because the data is public.

Red Pill

That was my wake-up call to start taking a serious look at DeFi. Since then, I've been learning by using several DeFi protocols. Some of them are simple; others are advanced. The space is only about two years old, so complexity is still prominent. However, builders continue to abstract complex features behind simple UIs similar to what fintech has done.

Here are some things you can do in DeFi today. Everything you'll read can be done in a few minutes (seconds if you have a funded wallet), not days or weeks. There are no middlemen and no humans in the process. Remember, your relationship is with code, not other people. It doesn't take weekends off and doesn't care about what you look like or how much money you have.

Providing AMM Liquidity

Retail investors learned a ton about investing after major brokerages prevented accounts from trading GameStop earlier this year. Investors learned about clearing houses, market makers, and payment for order flow (PFOF). Investors also learned that their trades are "free" because Robinhood gets compensated for routing orders to various marker makers.

These are institutional groups that provide liquidity to markets. Without them, spreads on trades will be too wide. Order books are used to match buyers and sellers, and market makers make money off the spread. Robinhood and other brokerages get a percentage of that spread. Say a trader wants to sell stock ABC for a minimum price of $1.11. Another trader is willing to buy ABC for no more than $1.14. A market maker facilitates this transaction and pockets the difference.

In DeFi, there are no centralized entities providing liquidity. There are no order books either. Instead, an Automated Market Maker (AMM) provides liquidity by helping traders swap tokens using various liquidity pools. Swapping is just like buying and selling. In our previous example, the user that sold ABC exchanged those shares for U.S. dollars. Things are more interesting with an AMM. Instead of trading ABC for USD and then USD for XYZ, users can swap ABC for XYZ instantly. Think of it as swapping your AAPL shares for MSFT without going into cash. This is possible because of AMMs — you don't need a buyer for every seller and vice-versa. Liquidity pools charge a fee for the service they provide. That fee is split between liquidity providers (LP) relative to their share of the overall pool. Anyone can be a liquidity provider.

As far as I know, there are no market maker pools in CeFi for retail investors. It isn't easy to coordinate it at scale. Rules and regulations also limit who is allowed to take such risks. Not everyone can provide stock market liquidity, but in DeFi, you can split 100 USDC ($100) into a 50/50 split of ETH/USDC and join a pool on any decentralized exchange (DEX). When someone swaps using your pool, you get a percentage of fees.

Lending & Borrowing

When you put your money in a bank, the bank puts that money to work. The interest you receive is what's left after they've taken their cut. Technically, loans create deposits, not the other way around. But for simplicity, let's say banks lend out deposits. There's often no visibility into what your money is being used for. When they make loans, you don't know where that money is going or what the collateral is. You don't even know if the loan is secured or not.

In DeFi, there are no banks. You can keep your crypto (volatile or stable) in a wallet and earn no interest, or you can lend it to others. With protocols like Compound or Aave, anyone can lend crypto and start earning interest immediately. Everything is transparent so that anyone can look up the collateral factor (how many cents a user can borrow after depositing a dollar worth of collateral).

Most DeFi loans are pooled together. When you lend your USDC or DAI, it can be collateralized by multiple crypto assets. There are protocols for those who want something more specific. For example, I love Sushiswap's Kashi because it isolates lending markets. You can choose what collateral you want your loan to be backed by. You can have your loan collateralized by ETH, BTC, or even governance tokens like AAVE. This means that you don't have to be directly exposed to it if you don't care much about bitcoin.

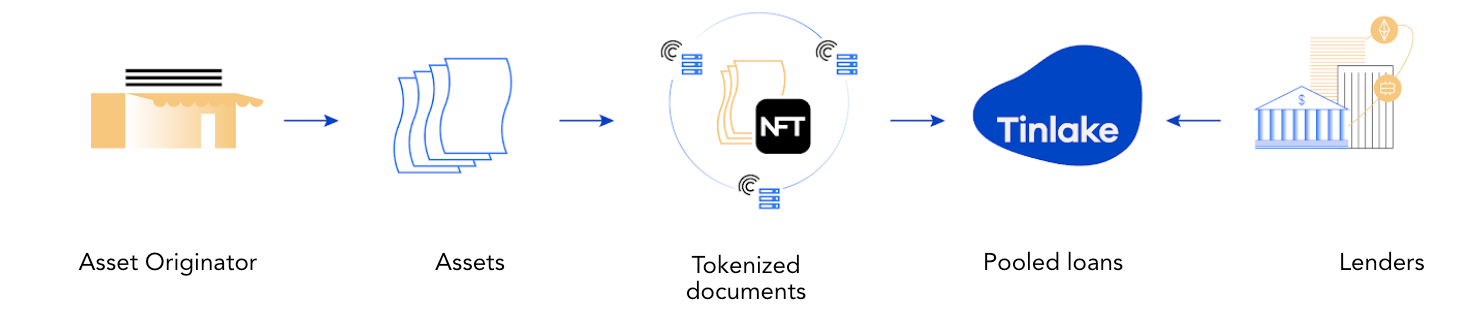

As long as you're able to put up collateral, you can borrow from DeFi protocols. Most loans are overcollateralized, and collateral is usually another crypto, but alternative forms are being developed. Say you don't have that many BTC or ETH to use as collateral, but you happen to own Jack Dorsey's first tweet that sold for $3 million. That NFT can be used to secure your loan on NFTFi. Other protocols like Centrifuge are tokenizing real-world assets like real estate into smart contracts. Like bonds, these loans have tranches, a fixed return (lower risk) senior tranche, and a variable return (higher risk) junior tranche.

Most DeFi loans have variable interest rates, but protocols like Notional focus on fixed-rate lending and borrowing. During extreme bull runs, you can lock in a high interest rate for a few months (as a lender) if you think the market will overheat. Borrowers can also take advantage of this when rates are extremely low. Fixed-rate lending stabilizes the ecosystem, so I want protocols like Notional to succeed. They recently announced longer-dated maturities allowing anyone to take out year-long fixed-rate loans by the end of 2021.

The most popular fintech name in p2p lending for retail investors was LendingClub. It closed its retail lending platform at the end of 2020 to focus on banking. Another name I've used in the past is Prosper, but it isn't fair comparing it to DeFi offerings. The 1% annual loan servicing fee that investors have to pay can't compete. That's on top of the lack of liquidity. In CeFi, your loans are locked till they are repaid. Fintech apps charge an embarrassing liquidity fee on top of other management fees to get around this. In DeFi, you can loan your money and take it out the next minute as long as there are funds in the pool. If all the funds are loaned out, it shows high demand, which translates to higher interest rates updated and applied to your old loans in real-time.

Fintech has some good offerings when it comes to borrowing against your stock market portfolio. But that's about it. Services that let retail investors borrow against their real estate holdings offer terrible deals. Most want a piece of the equity (which is ok), but none of the maintenance or repairs (which make no sense). What about pokemon cards and other collectibles? DeFi has made more remarkable strides to collateralize these in its two years of existence than fintech has in a decade.

Liquidation

When a borrower's loan to value ratio drops below the collateral ratio, their position can be liquidated. Say you borrow $1 of USDC backed by $1.5 of ETH. If the price of ETH drops, so does your collateral. If it is below the collateral ratio, your loan becomes unhealthy, and liquidators can step in and act as a backstop. They can repay the lender and get a nice discount on the collateral.

You guessed it. You can liquidate unhealthy loans. It's weird getting excited during crashes, but I had fun watching liquidations when crypto crashed in May. In TN09, I wrote:

When Archegos blew up, prime brokers liquidated and traded the remaining assets within themselves (institutions/hedge funds). When a decentralized crypto account blows up, anyone, even you and I, can bid for what's left of the account.

You can do all the hard work or have your money do it for you. With protocols like KeeperDAO, you can act as an LP for liquidators and earn fees for doing so. This means that market participants are the final backstop (for non-fiat backed tokens). It's a lot different from what we've come to expect in the stock market, where the central bank acts as a backstop. Market crashes recover when investors feel like buying, not when artificial liquidity is infused in the system. Some need the Fed's assurance, but those that don't can capitalize on the risk premium. But that's a topic for a different post.

Yield Farming & Governance

Liquidity providers, lenders, and even borrowers are rewarded for using various protocols. Since information and access are open to everyone and spreads are arbitraged across exchanges, rewards are how protocols compete for users. It's like getting a little piece of Robinhood every time you use the app. The reward tokens are essential — they represent ownership, among other things.

For example, I received some COMP tokens for lending on Compound last year and forgot about them. Last week, Compound launched a product that'll allow neobanks and other fintech firms to leverage the power of DeFi to boost their returns on deposits [3]. Similar to what happens when a public company launches a promising product, the price of COMP spiked on the news. Protocol governance tokens are like shares in a company.

Another token I've earned is SUSHI from Sushiswap. This one rewards holders with something akin to a dividend. When people swap tokens on the protocol, a 0.30% fee is charged. 0.25% of that goes to the LPs, and the remaining 0.05% is distributed to SUSHI holders that have staked their coins. Like dividends, earnings are distributed to holders. Unlike dividends, earnings are paid in real-time and compound automatically.

Yield farming consists of lending, borrowing, staking... basically leveraging anything DeFi has to offer to generate additional yield. The reward tokens protocols distribute can be staked or used as collateral for other loans and so forth. You can use spreadsheets to figure out how to maximize yields or, you guessed it, there are protocols for that. Yearn Finance, for example, automates and abstracts all the complexities of yield farming.

The concept of users being owners is absent in CeFi. Robinhood is making strides by attempting to reserve some of its shares for its users. Airbnb also allowed hosts to buy shares during its IPO. But if it were in DeFi, hosts would have been accumulating shares from day one. It's an odd concept, but what if you got some VISA for every swipe or UBER for every ride? Decentralized Autonomous Organizations (DAOs) can reward users like this because they are more efficient businesses with little to no humans at the core. More on that later.

Reward tokens often act as governance tokens. In CeFi, retail investors know they get a piece of a company, but many don't vote with their shares. Voting on leadership or compensation isn't appealing for many retail investors. With DAOs, token holders get to vote on everything from features and support to grants that fund other projects. Seriously, more on DAOs later.

DeFi x FinTech

These are some of the things that are exciting about DeFi. Till now, I've framed most of the discussion as fintech vs. DeFi, pitting both against each other. The reality is that things won't turn out this way. DeFi won't kill fintech but rather improve it. Fintech apps like BlockFi leverage DeFi to offer 8% APY on USD. Users don't have to learn about any of the protocols I listed above. They can deposit some cash and earn by the second. BlockFi is centralized — you can tell which crypto services are centralized or not by asking: "do I own the private keys to my wallet?" — but it is better at onboarding new users. This is good news because most users want DeFi economics minus the complexity.

FinTech will slowly swap out legacy infrastructure for DeFi protocols. We can't get a DeFi mortgage yet, but we're getting there. Everything money-related is moving on-chain, including insurance for hacked or buggy protocols (see NexusMutual). There are risks to using DeFi, but there are risks in every system. The difference here is that people are allowed to decide which risks they want to expose themselves to.

People in rich countries like the U.S. with somewhat stable currencies can attempt to ignore DeFi's impact, but people living in countries where their paycheck is worth much less before the next one hits can't. Those people are actively preserving their wealth by converting their savings to USDC. Better yet, they're growing it. They can save in a foreign currency without paying crazy conversion fees. Centralized finance is plagued with unnecessary fees and intermediaries. Software, in the form of smart contracts, is disrupting brokers in the finance industry.

Regulation is still a big question mark, but FinTech will help fight for DeFi on behalf of users. As I mentioned in part 1, finance loves technology when it increases the speed and fluidity of money. I'm not sure where DeFi is going, but I have an idea where CeFi is headed.

I plan to write more on regulation, and how fintech might integrate with DeFi. I'm also following central bank digital currency (CBDC) activity very closely. My goal with this is to convince you to stop closing every article that mentions crypto. The space is worth paying attention to.

Sources

[0] a16z Crypto Fund III — https://a16z.com/2021/06/24/crypto-fund-iii/

[1] Hwang Leverage — https://www.nytimes.com/2021/04/03/business/bill-hwang-archegos.html

[2] Iron Finance Post Mortem — https://ironfinance.medium.com/iron-finance-post-mortem-17-june-2021-6a4e9ccf23f5

[3] Compound Treasury — https://www.coindesk.com/compound-labs-launches-treasury-to-get-big-firms-reaping-defi-yields