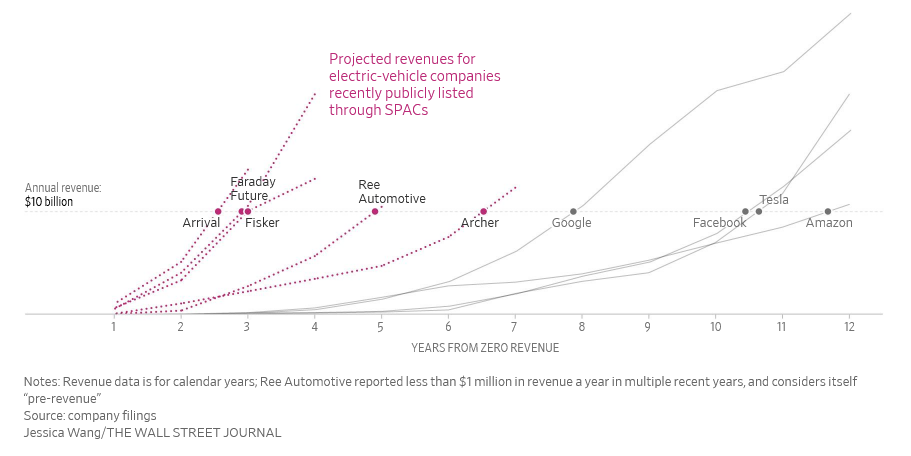

EV SPACs With Empty Revenue Promises (TN04)

EV companies with nothing but reservations are promising to rake in over ten billion dollars in less than seven years.

I have an announcement to make. I’m switching the direction of the newsletter. Instead of delivering the content via old-school email, it’ll now be delivered via hologram. I don’t have the tech or the resources to make it happen, but you can trust me. I’m Tolu, the CEO of a recent newsletter SPAC that plans to reach $10b revenue in 3 years. We have $0 now, but imagine the potential!

They Can't All Be Winners

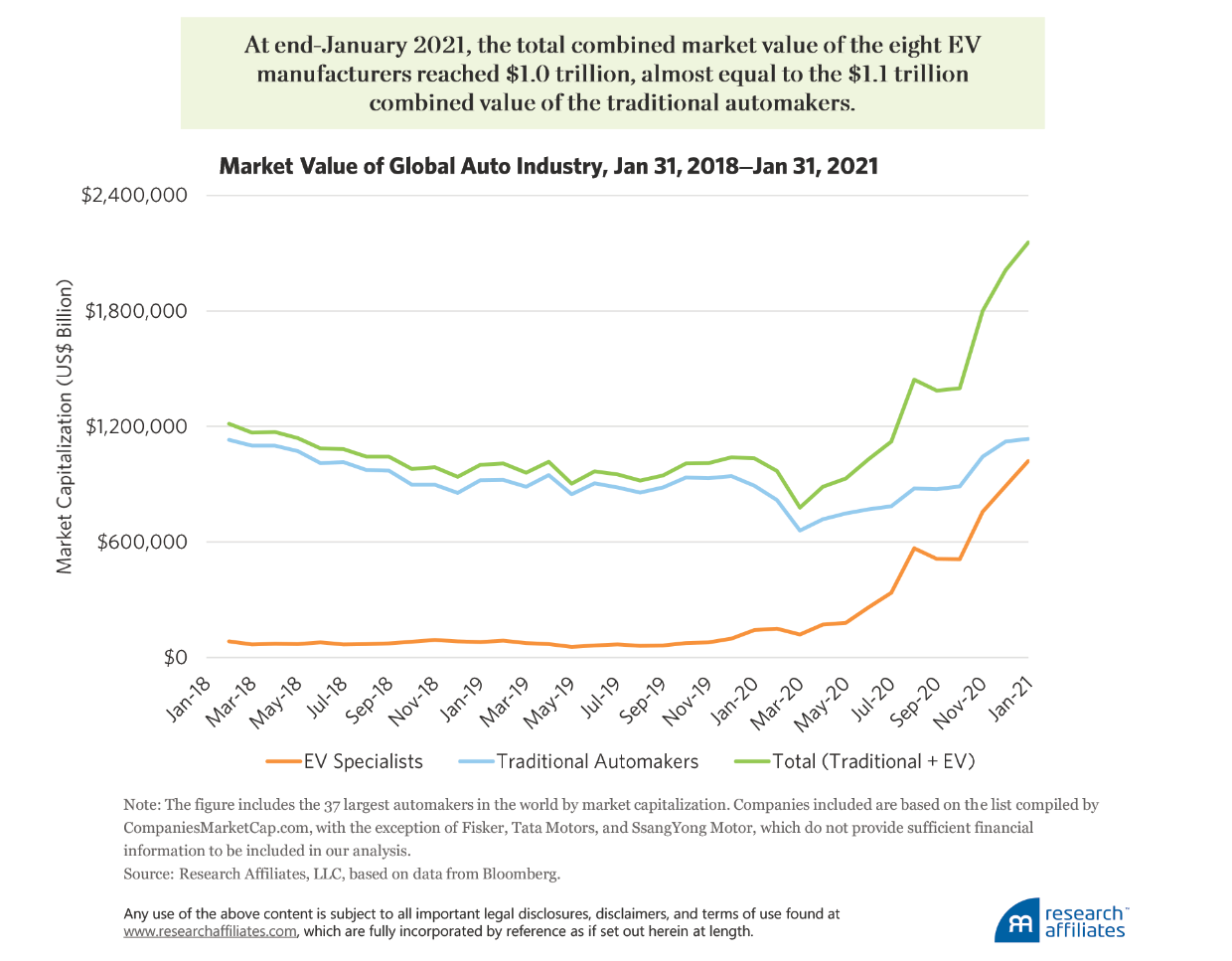

I’m always puzzled by how investors can be so gullible. A few short years ago, no one wanted to invest or touch electric vehicles. Many founders weren’t even interested in the space because capital was scarce. Now it seems like every other popular SPAC is for an EV company. These companies have a few things in common. They have little to no revenue, but they have big dreams. These EV SPACs are promising explosive revenue growth. It’s OK to dream big, but these dreams are meant to be just that…dreams.

Some of these SPACs promise to go from less than $1 million in revenue to $10 billion or more in less than eight years. Some are even promising to hit it in three years or less. Investors love it. We see more of these EV SPACs because investors continue to reward these companies. The market believes that the traditional automakers looking to make a turnaround, the established EV-only companies, and most of the new EV SPACs will succeed. This is highly unlikely.

A few of these companies promise to beat Google’s record for their first $10 billion in sales even though they are in direct competition with themselves and the traditional automakers that are now investing in EVs. This scenario is known as the Big Market Delusion. The assumption these entrepreneurs and their investors are making is that the EV market will be big enough for most of these companies to coexist. They are probably right. EVs may take over, but not at the rate they are promising. I’ve probably said it a thousand times by now, but disruptive innovation does not equal disruptive returns for investors. I believe EVs are here to stay. Like the railroad and the internet, EVs are not going anywhere. But similar to the railroad and the internet, most of these entrants have to fail.

You’re going to need a lot of luck if you’re trying to find the next Tesla. There’s so much capital chasing EVs at the moment that it has become a self-reinforcing loop. It lures more investors in as share prices continue to get bid up. I’m not sure if we’re in an EV bubble, but Nikola was once worth $21.5 billion on zero revenue. That’s not fair. They brought in about $95 thousand in 2020.

Weekly Chart

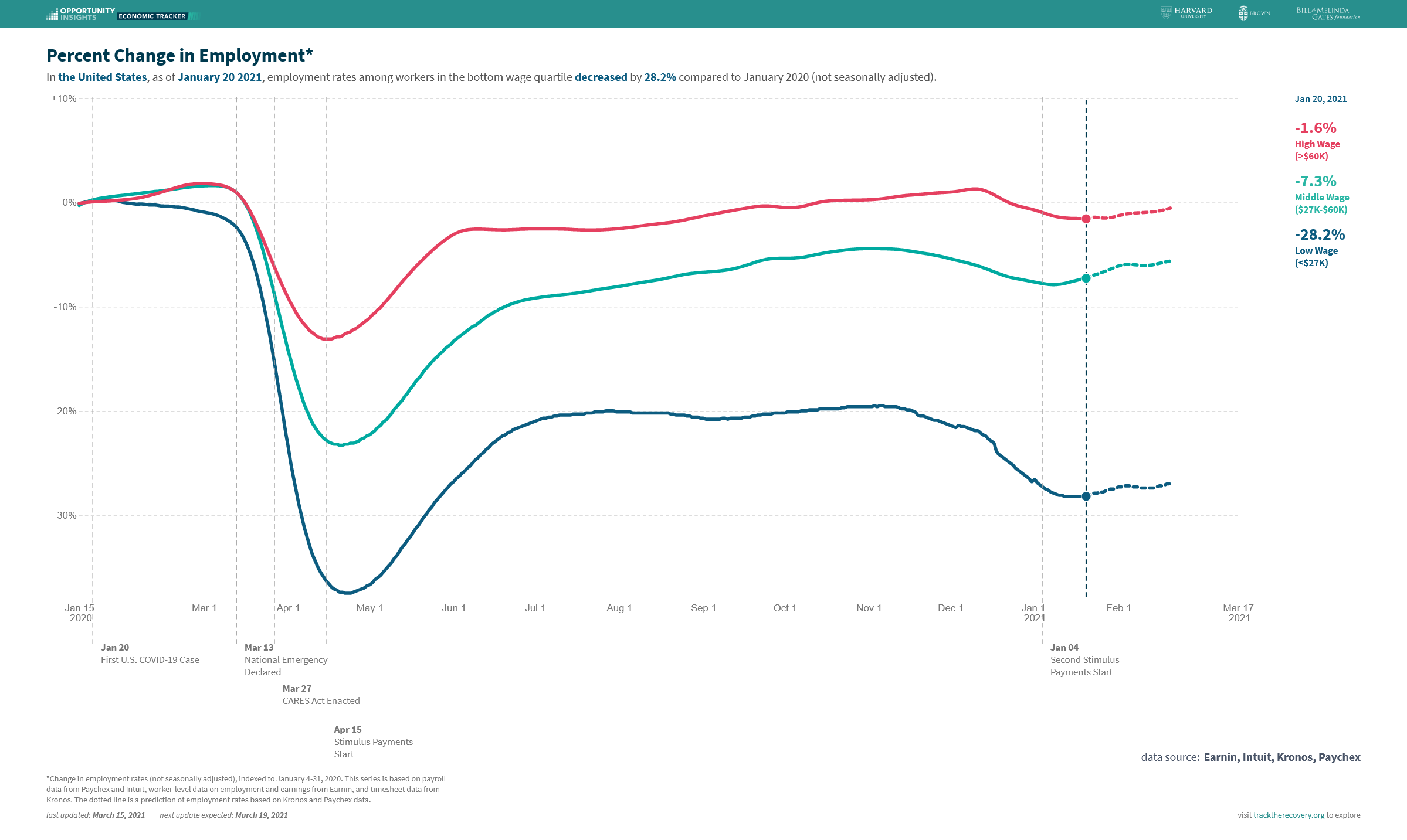

Unemployment is almost back to pre-COVID levels for high-wage workers, but things aren’t looking good for low-wage individuals. My latest YT video dives into these numbers. Why Americans are saving so much money, and what that might mean for the recovery.

What to Read

There are many things of note in the memo, but my highlights were the following paragraphs.

The biggest risk of all is the possibility of rising interest rates. Rates have declined quite steadily for the last 40 years. This has been a huge tailwind for investors, since a declining-rate environment lowers the demanded returns on assets, making for higher asset prices. The linkage between falling interest rates and rising asset valuations is a good part of the reason why p/e ratios on stocks are above average and bond yields are the lowest we’ve ever seen (which is the same as saying bond prices are the highest).

But the downtrend in rates is over (if we can believe the Fed’s assurance that it won’t take nominal rates into negative territory). Thus, while interest rates can rise from here – implying higher demanded returns on everything and thus lower asset prices – they can’t decline. This creates a negatively asymmetrical proposition.

I’ve discussed interest rates a few weeks in a row now. I’ve written and made YT videos about it because it is somewhat of a big deal. I would also like to highlight something HM didn’t touch on. There’s a non-negligible chance that the economy does exceptionally well, better than the Fed is expecting. If this were to happen, the Central Bank might have to fast-track its rate-hike timeline. That move will likely disrupt current high market valuations. But not all companies have high valuations. They may all fall, but some will fall less.

What to Watch